Everyone knows George Soros as the man who “broke the Bank of England.” But nobody has ever explained why his trade worked. How could a single hedge fund manager bring down one of the most stable currencies in the world? The history of Britain vs. Soros reveals what happens when a country turns itself into a colony by pegging its currency to another.

To understand how Soro’s trade set up, we have to look at a brief economic history of Britain in the 1980s. After years of high inflation in the 1970s, Margaret Thatcher came to power promising to privatize government-controlled industry and limit labor unions. Her goal was to make England more competitive in the world economy, lower inflation, and revive “the sick man of Europe”.

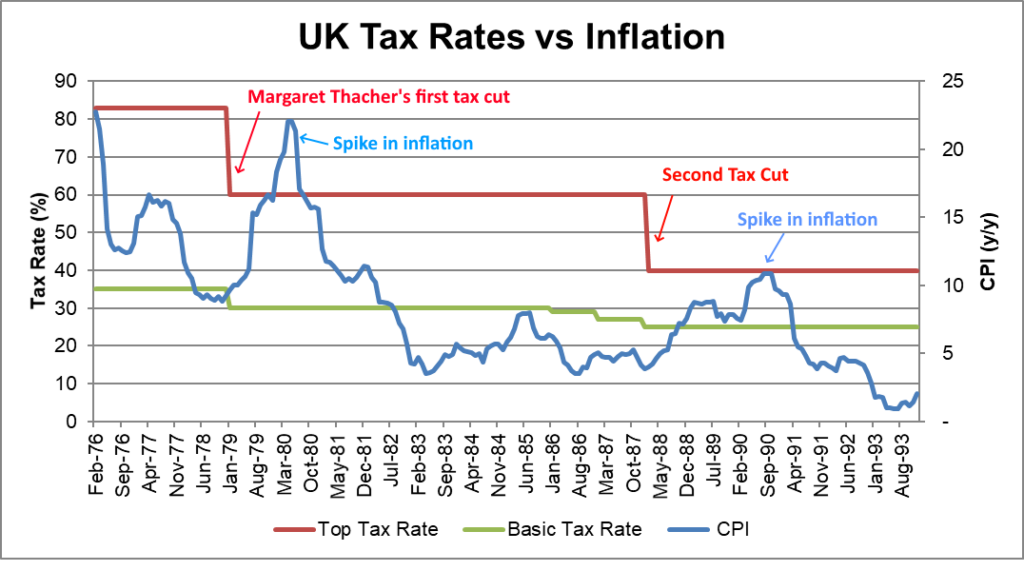

While controversial and painful, her policies eventually had the desired effect. In addition to privatizing British Petroleum and British Telecom, Thatcher’s government broke the coal miner’s union in 1984. The cost of a more competitive industry and weaker labor unions was higher unemployment. Unemployment in England initially spiked to 12% before falling back to 7%. Painful, but Thatcher got what she wanted. Inflation came down from 15% to 5% in 1983.

In contrast to her deflationary policies, Thatcher tried to re-envigorate growth with large tax cuts. In 1979, Thatcher’s government cut upper-end tax rates from 80% to 60%. Cutting taxes can increase inflation because it leaves more money in the economy (“If The Government Can Print Money, Why Do We Pay Taxes?“). This first tax cut had some inflationary effects but the economy was growing slowly so the spike in inflation was transient.

However, the tax cut policies were taken too far in 1988. The government threw gas on the inflation fire by lowering top income tax rates from 60% to 40% while the economy was already growing over 5%. The government cut tax rates when it should have been increasing them. In the late 1980s, Britain experienced inflation of over 10% in 1989, led primarily by a booming housing market.

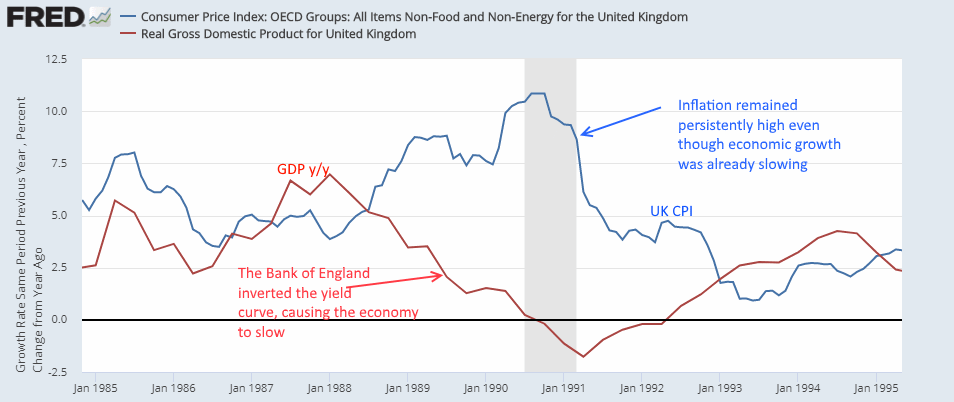

In response to the spike in inflation, the government raised short-term interest rates to slow the economic growth, eventually driving Britain into a recession in 1990.

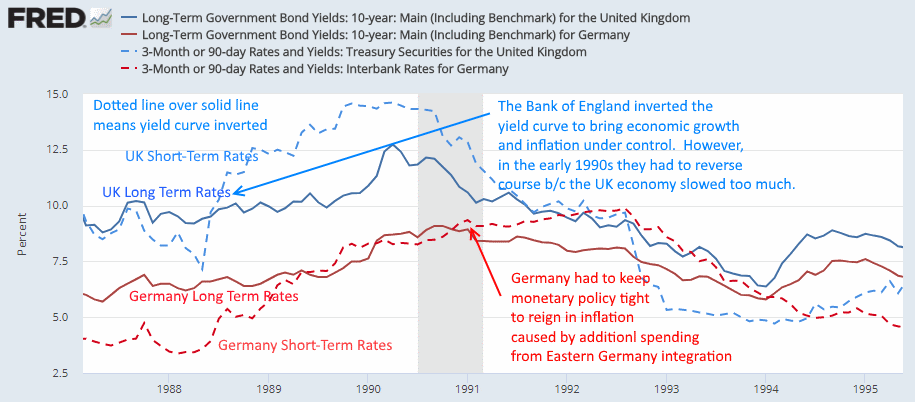

Despite the economic slowdown, inflation remained persistently high. To reign it in, Prime Minister John Major decided to join the European Exchange Rate Mechanism (ERM) in October 1990. This seemed like a reasonable solution to the Prime Minister because of Germany’s ironclad post-WWII history of controlling inflation.

However, it turned into a disaster for Britain.

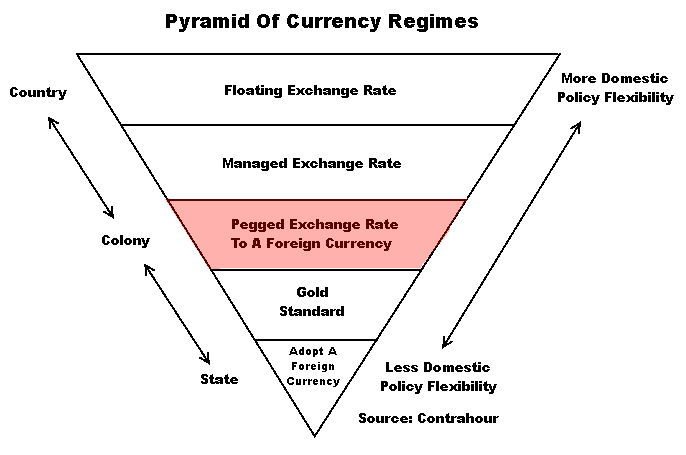

The ERM was a currency union by eight countries to help stabilize trade and currency fluctuations. Each country’s central bank maintained its currency within a tight trading band to the other currencies by buying and selling foreign currencies. And Since the ERM was weighted toward the Deutsche Mark, each country in the ERM basically pegged their currency to the Mark.

In joining the ERM in 1990, Britain also pegged the Pound to the Mark. Even though Britain had its own sovereign currency, its own ability to tax, and its own bond market, Britain adopted the monetary policies of Germany. Instead of simply using its own policy tools to reduce inflation by raising taxes, Britain turned itself into a colony.

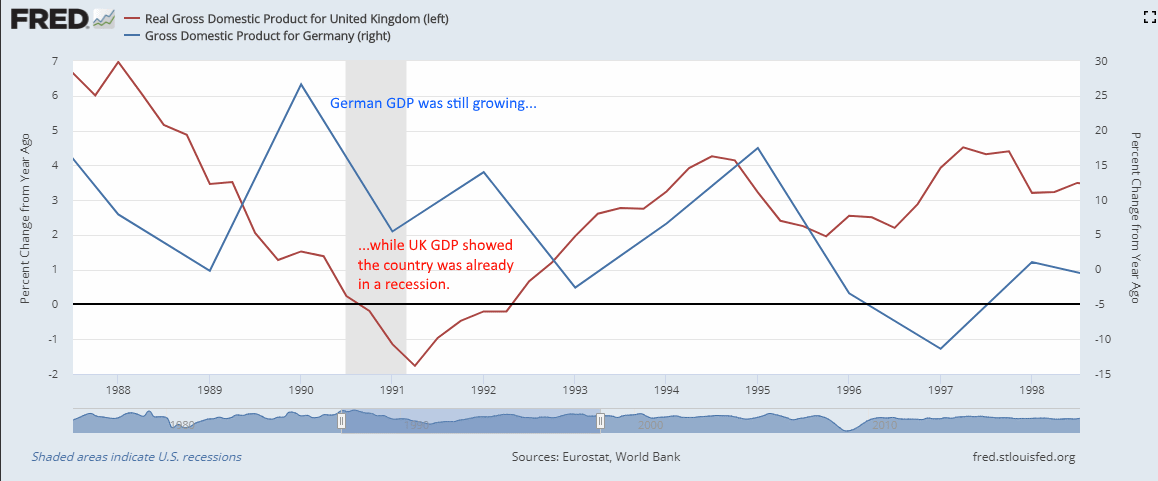

The problems of pegging Britain to a foreign country’s currency became apparent almost immediately. While Britain was dealing with a slowing economy, Germany was experiencing record growth. Germany had been spending to re-integrate East Germany and needed to keep monetary policy tight to reign in inflation. But the United Kingdom was already in a recession and needed expansionary monetary and fiscal policies.

This dichotomy turned out to be a huge problem for the Bank of England and gave George Soros his opportunity.

A free-floating currency is the “pressure release valve” of a country’s monetary and fiscal policies. All things being equal, when a country’s economic growth slows, the currency declines as well. But in the case of the Mark and the Pound, the two currencies couldn’t unlink because the UK had joined the ERM the year before. And the ERM required the Bank of England to maintain the Pound within a 3% +/- range with the Mark.

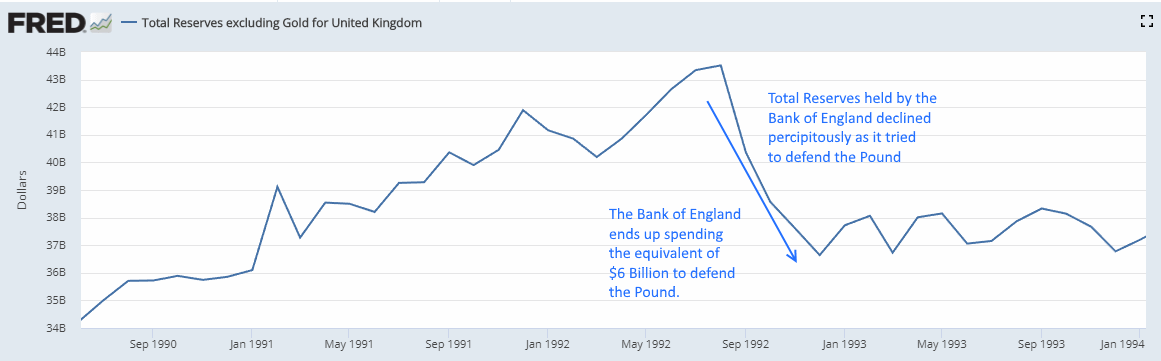

Any good trader will tell you the first maxim of trading is “don’t fight the market.” And the Bank of England was fighting the entire world. The global market sold Pounds as the UK economy weakened and, likewise, bought Deutsche Mark as its economy remained strong. To maintain the peg, Britain needed to obtain the foreign currency it had pegged to. So, to buy Pounds in the market, the Bank of England needed Deutsche Marks. Typically, this wasn’t a problem. In fact, the Bank of England had the equivalent of 40 billion in foreign exchange reserves to defend the Pound.

However, in the trillion-dollar currency market, 40 billion is not a lot of money.

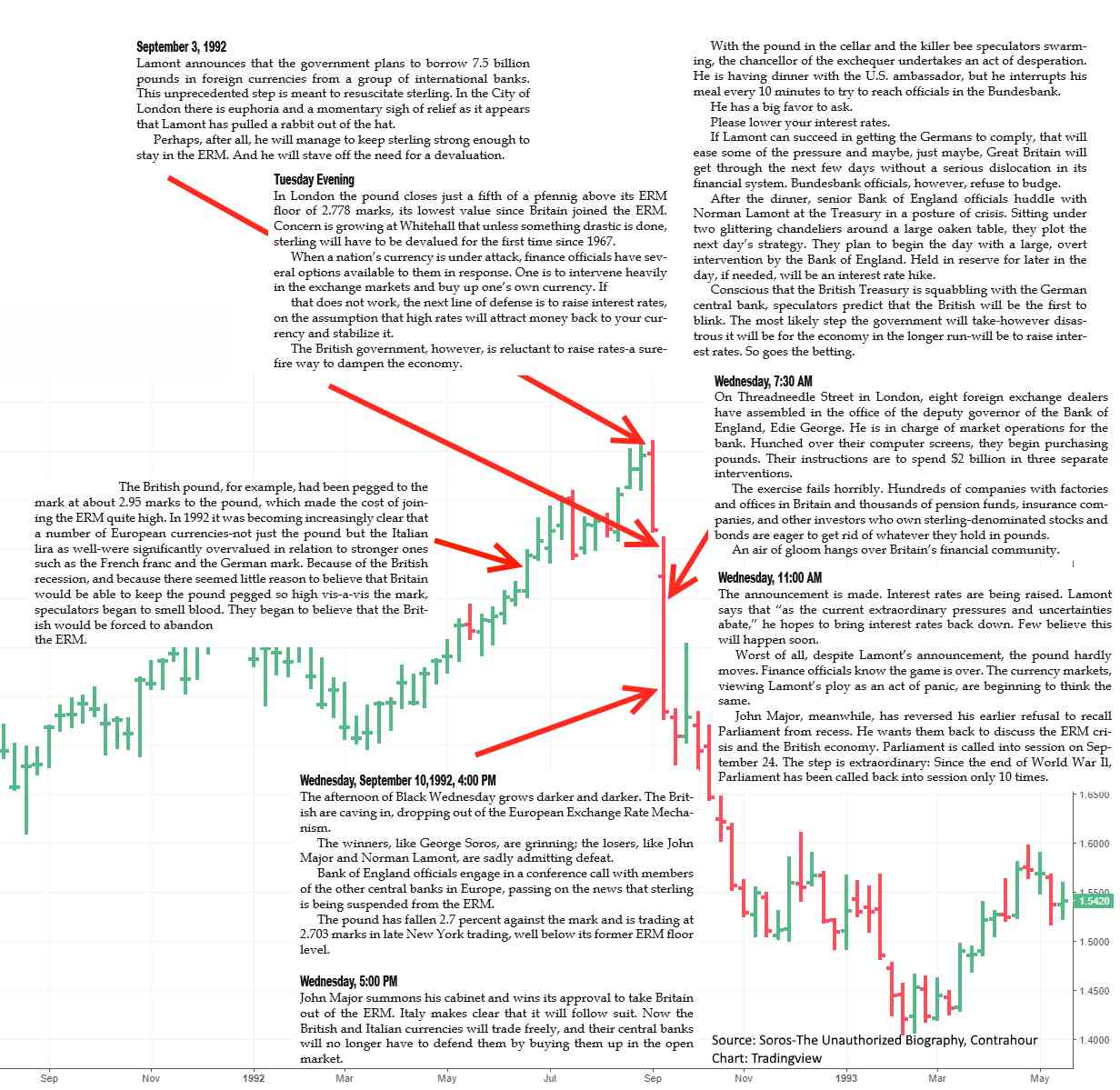

The Bank of England knew it was in a difficult situation. A week before the crisis hit, the Bank of England borrowed 7.5 billion in foreign currency from a group of international banks. But even this turned out not to be enough to defend the Pound. George Soros’ fund, by itself, was short 7 billion Pounds.

The following chart of the British Pound during 1992 highlights the sequence of events overlayed with explanations from “Soros: The Unauthorized Biography.” In short, once the Pound started falling and traders piled on, the Bank of England quickly started running out of foreign currency reserves. Within two weeks, the Prime Minister went from defending the ERM to leaving it.

This is how George Soros was able to take down the Bank of England. Although Britain had its own sovereign currency, the country had pegged its currency to the German Mark. That meant it needed foreign currency reserves to maintain the peg. The Bank of England literally had to spend billions of German Marks to defend its currency. Soros realized that the British government didn’t have enough reserves to maintain the peg and would have to abandon it if the Pound began to sell-off.

All in all, it’s estimated the Bank of England spent 6 billion on its futile defense. That was real money England could have used to import goods from Germany. One British newspaper noted that England spent as much maintaining the Exchange Rate Mechanism as it did on fighting the Gulf War. This, of course, was a politically unfeasible position. Two years later John Major lost the Prime Minister election because of the ERM debacle.

The most amazing part of the whole episode was the outcome. Namely, nothing. The Pound settled into a long trading range that lasted the remainder of the decade. And the devaluation of the Pound ended up being a benefit to the economy because it helped spur exports. GDP growth accelerated and unemployment continued to decline until 2001.

But not understanding that a country can regulate inflation through taxation cost England six billion in foreign currency reserves, real money that had a real quality of life repercussion for its citizens.

1 thought on “Everything You Know About Economics Is Wrong: How Soros Broke The Bank Of England”

Comments are closed.