A lot of the kids (well…one) have come up to me in 2021 and asked:

“Uncle Contra, Uncle Contra…how will we know when this tech bubble reaches a top?”

And I say…”Well, children, my bubble-top-calling days are over. But take a look at this handy checklist I posted back when I called the top (nearly) of the China Shanghai market in May 2007.”

Spongebob: Patrick, check it out!

Patrick: Wow!

Sponge & Pat: Hooray! Bubble party!

Thug: Hey! Who blew this bubble? You all know the rules!

Thugs: [in unison] All bubble-blowing babies will be beaten senseless by every able-bodied patron in the bar

It’s almost impossible to call the end of a stock bubble but there are several key indicators that investors should monitor when trying to time an exit from a bubble.

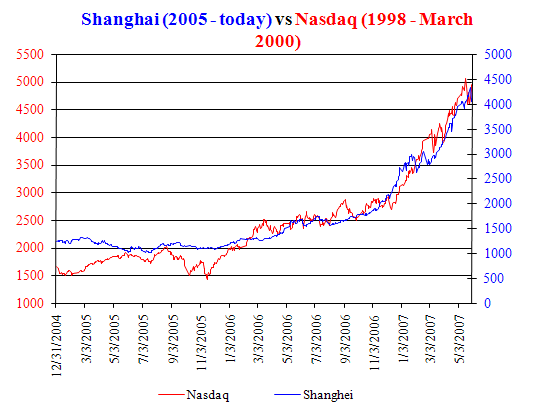

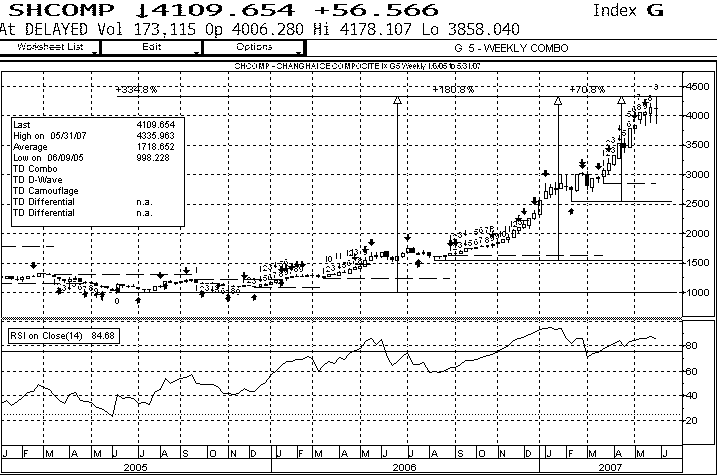

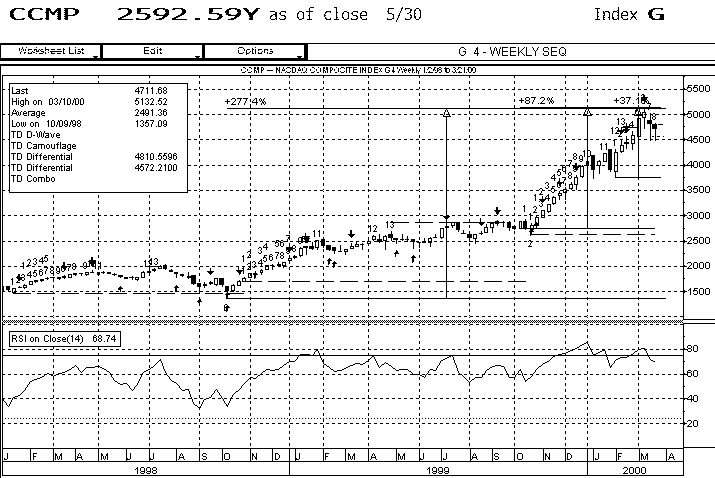

Use this handy-dandy checklist next time you think you see a price bubble forming and want to call a top. I’m going to look at the most over-exuberant market, the Shanghai Composite Index (DJSH) to see if the recent 180% run is getting a bit “extended.”

1. Parabolic Price Increase

1. Parabolic Price Increase

This one’s pretty obvious since parabolic price increases are the definition of a bubble. We’ve had so many examples of bubbles now that it’s getting pretty easy to spot the crazy price action that marks the final phases of a stock bubble advance. And all bubbles should be compared to the granddaddy of all bubbles – the NASDAQ from 1998 to 2000. The Shanghai’s parabolic advance looks very similar to the Big Nasdaq.

Amazingly, the current advance in Shanghai makes the NASDAQ blow-off look tame. Since the beginning of the move in 2005, the Shanghai has advanced 335% vs the 1998 – 2000 advance of the NASDAQ of 277%. The final acceleration higher in the NASDAQ from October 1999 to March 2000 went up 87%. The current blow off in Shanghai from September to today has registered a 180% increase. The current parabolic move in China is truly historic because, at the time, the NASDAQ bubble had been the biggest bubble move ever.

Here’s the three-year chart of the Shanghai composite…

Chart Courtesy Bloomberg

…versus the NASDAQ composite from 1998 to 2000.

Chart Courtesy Bloomberg

2. Strong Indexes Mask Underlying Weakness

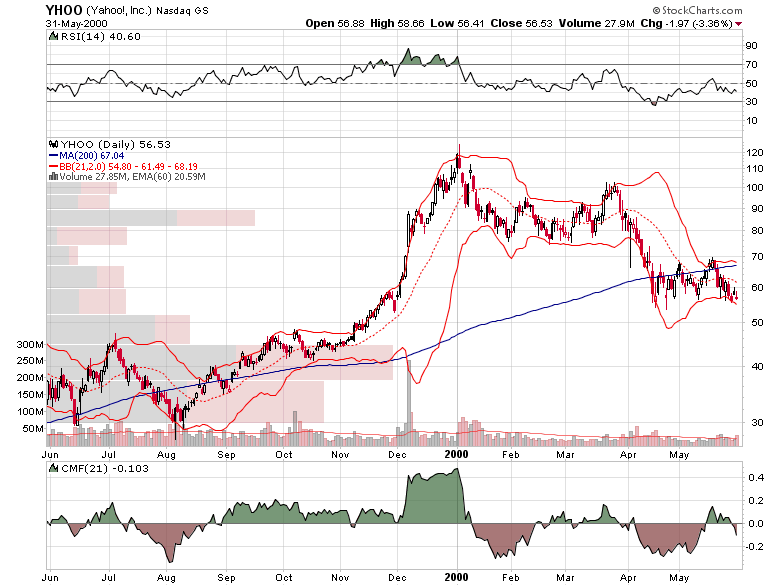

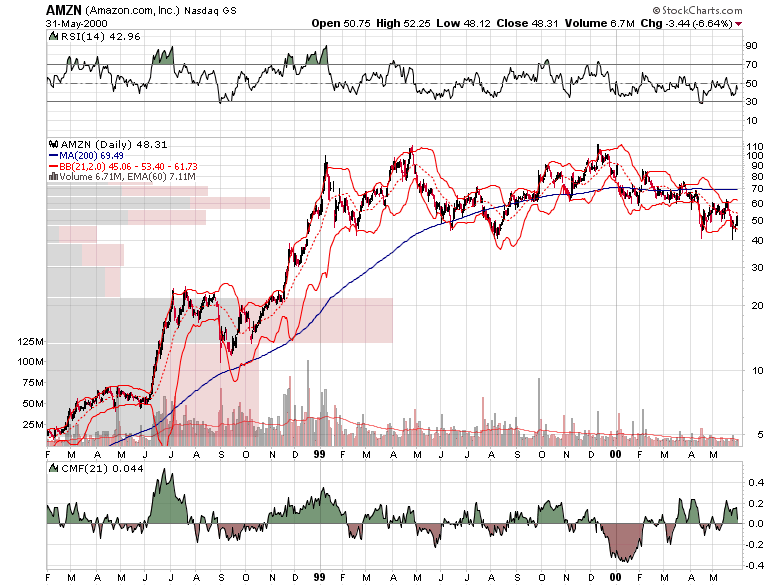

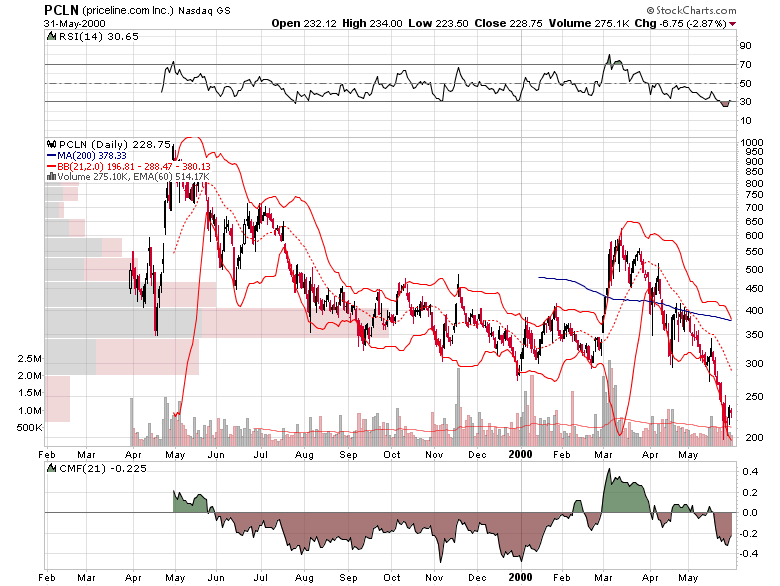

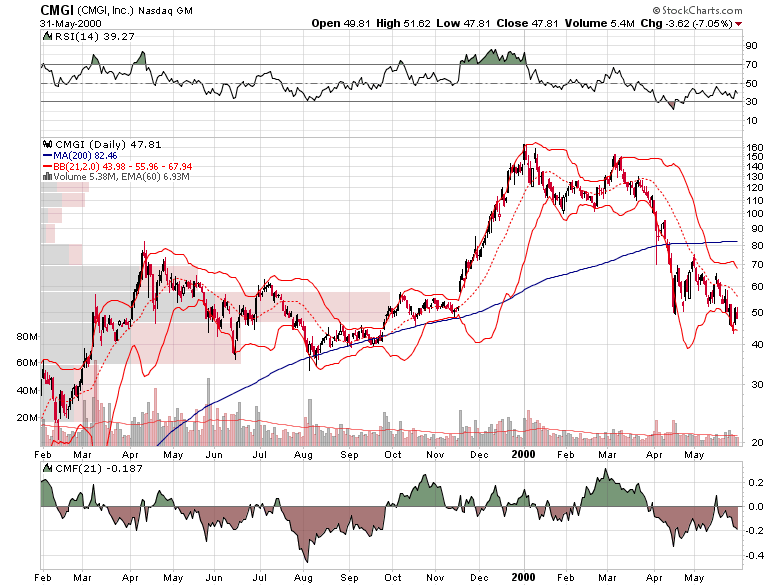

During the final stages of a bubble blow off, most stocks have already peaked out and are beginning to head down. Here’s a snapshot of some of the leading Internet stocks from 1999 to 2000. You’ll notice that none of them were hitting new highs with the NASDAQ in March 2000.

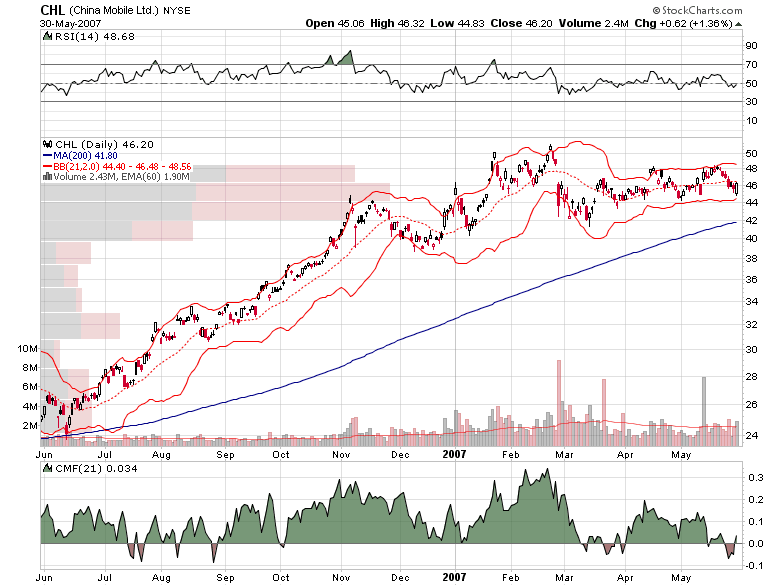

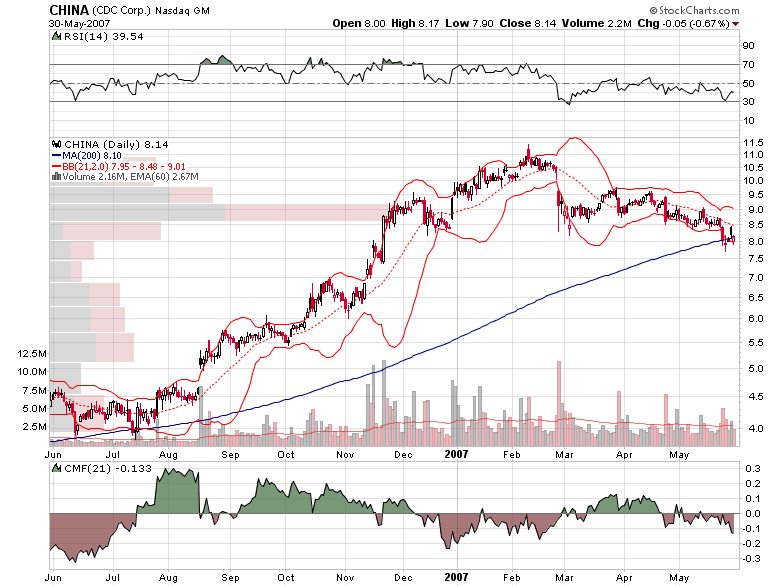

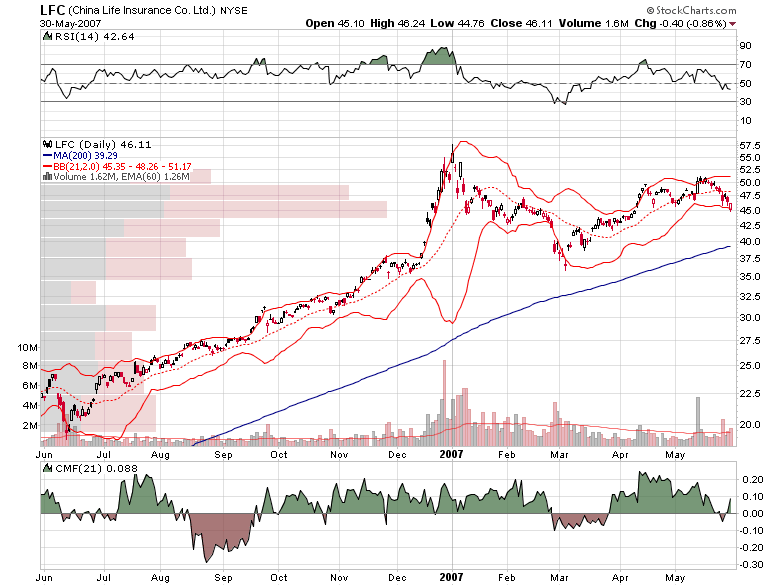

Here’s a snapshot of some leading China stocks right now.

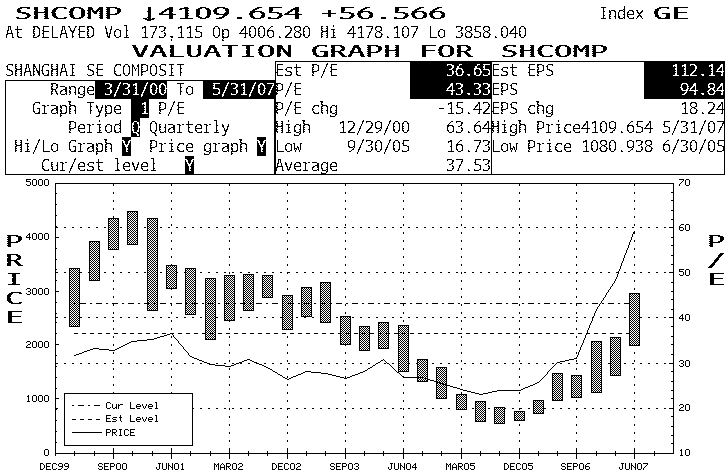

3. Valuations Are Off The Charts

In 2000, Cisco traded at 180x trailing earnings and 40x sales. Amazon traded at 100x sales and had no earnings. eBay traded at 1000x sales and had no earnings. In the Tokyo real estate bubble in the late 1980s, prime real estate went for as much as $100,000 a square foot. Now that’s a bubble valuation.

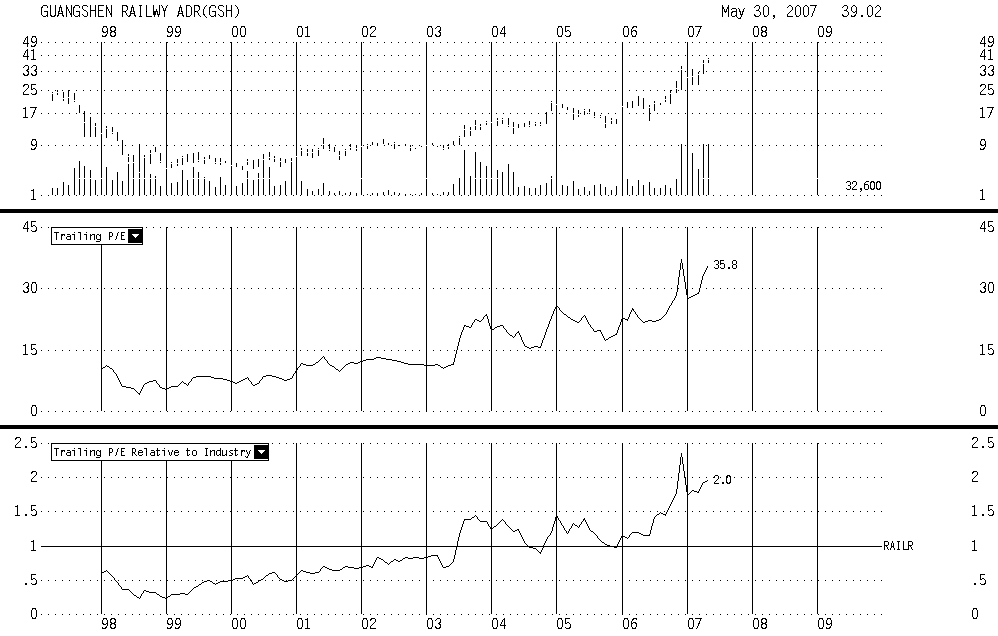

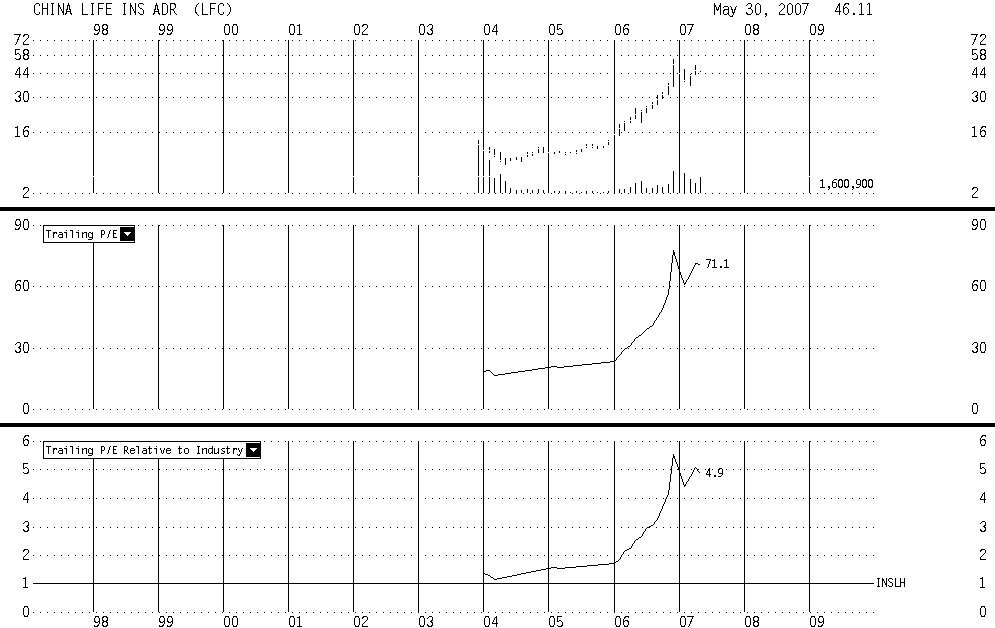

In comparison, many China stocks look downright cheap. While a couple of outliers like China Life (LFC) and Guangshen Railway (GSH) trade at well above average multiples and are approaching bubble valuations, many China stocks are simply trading at slight premiums to their industries.

China Life and Guangshen Railway look expensive…

Chart Courtesy Baseline

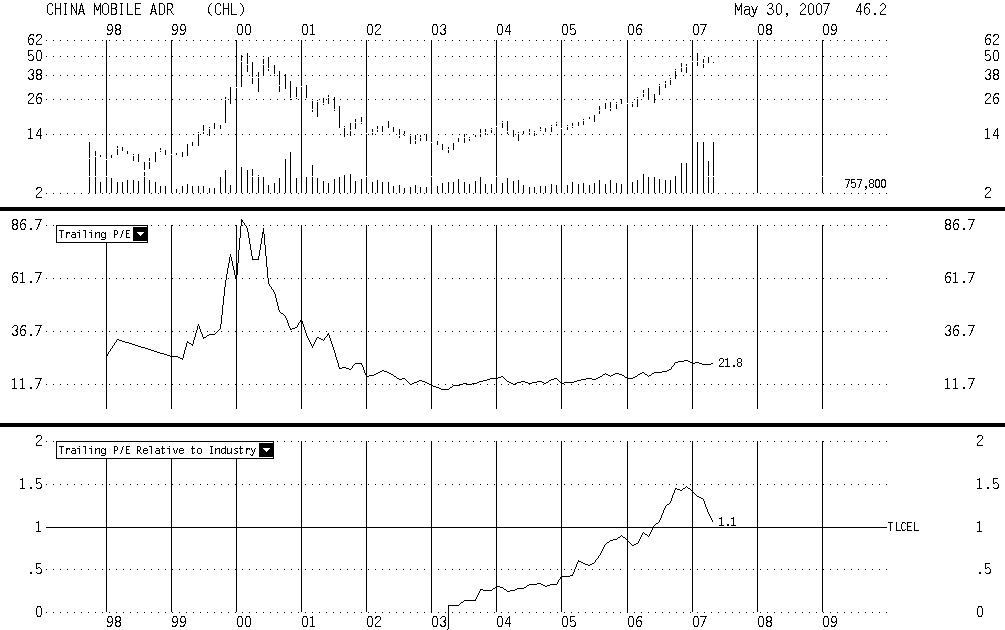

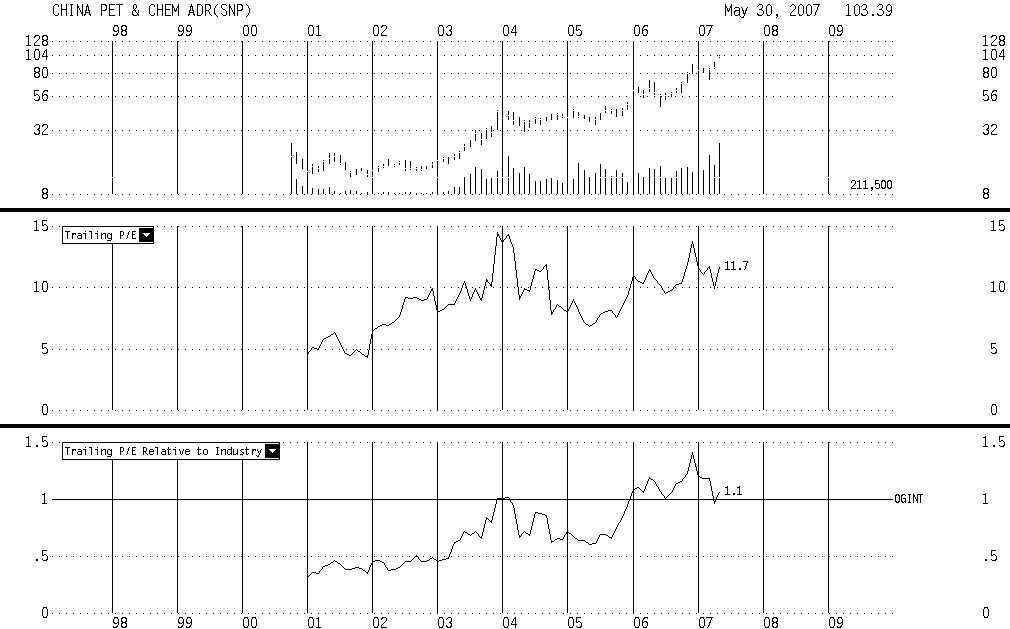

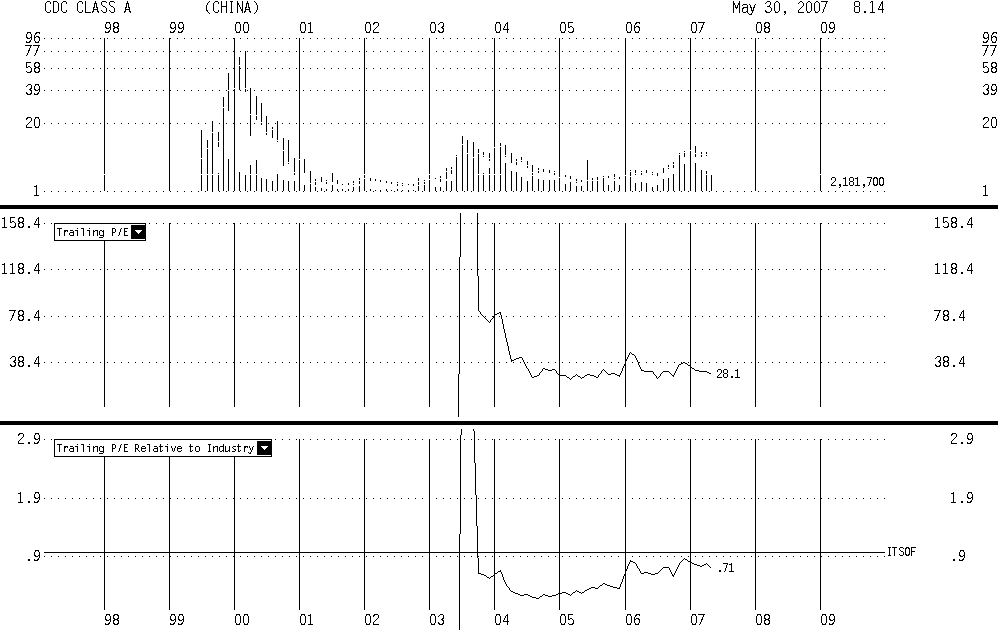

…but China Mobile (CHL), China Petroleum (SNP) and others are trading in line with their industry multiples despite the huge stock price advance.

Chart Courtesy Baseline

The overall Shanghai market is trading at about 43x earnings, which, while expensive, isn’t at the highest level ever.

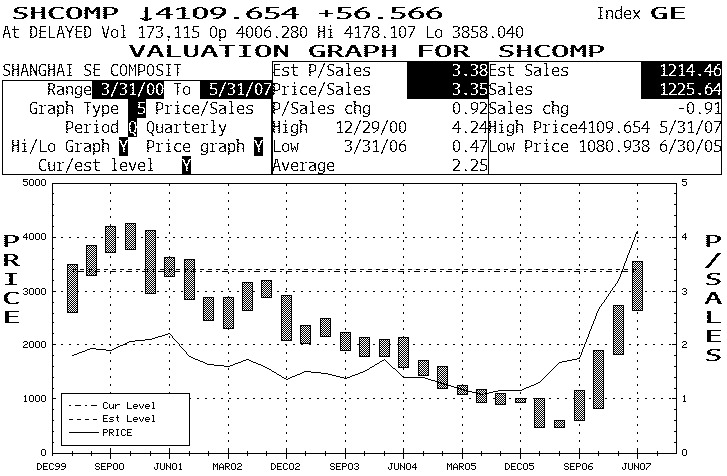

The price to sales ratio shows a similar pattern.

Chart Courtesy Bloomberg

4. Retail Investors Are All-In

In 1929, retail investors flocked to bucket shops to trade $200 of stock on $1 margin during their lunch hour.

In 1999, lawyers and doctors quit their jobs to trade stocks at day trading firms.

In 2007, Chinese are quitting their jobs to trade stocks. Over 27 million brokerage accounts have been opened in 2006 bring the total to well over 100 million.

From Chinadaily.com…

Xiao Feng, a former investment consultant at a futures company in Nanjing, put his three apartments and two vehicles – worth 5 million yuan – up as collateral days ago to get a 10 million yuan loan to invest in the stock market.

But the cost of borrowing is high – with an annual interest rate of 25 percent, he’ll have to pay the lender 2.5 million yuan in interest at the end of the year, reported the Nanjing Morning Post on Wednesday.

In addition, the lender will monitor his stock trading account. If the value of Xiao’s portfolio drops below 8 million yuan, the lender will liquidate his stock holdings to prevent a further decrease in the principal, spelling a loss of two million for Xiao.

When the 2.5-million interest payment is also taken into account, Xiao Feng will lose what he has worked for in the past 10 years – all his collateral.

Then why take such a risk? “Maybe it is the lure of the stock market. If an investment in a stock triples, or quadruples in a short period, then why not try?” he replied.

No wonder the Chinese government is so concerned. The road to capitalism will get much bumpier if people actually start getting a sense of risk and lose money. It will be an in vitiation for more, not less, government intervention – if that’s even possible in a communist country.

So, three out of four on the Bubble Top Checklist are definitely confirmed, and one is not. That’s probably close enough to call for a significant “correction”. Tomorrow, I’ll take a look at how US investors might be able to make some money off of the China stock bubble “correction”.