Spongebob: Patrick, check it out!

Patrick: Wow!

Sponge & Pat: Hooray! Bubble party!

Thug: Hey! Who blew this bubble? You all know the rules!

Thugs: [in unison] All bubble-blowing babies will be beaten senseless by every able-bodied patron in the bar

It’s almost impossible to call the end of a stock bubble but there are several key indicators that investors should monitor when trying to time an exit from a bubble.

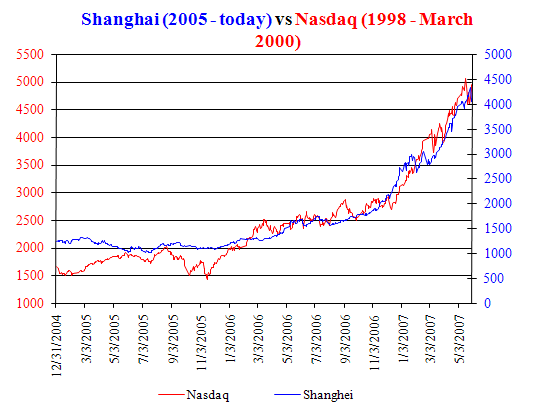

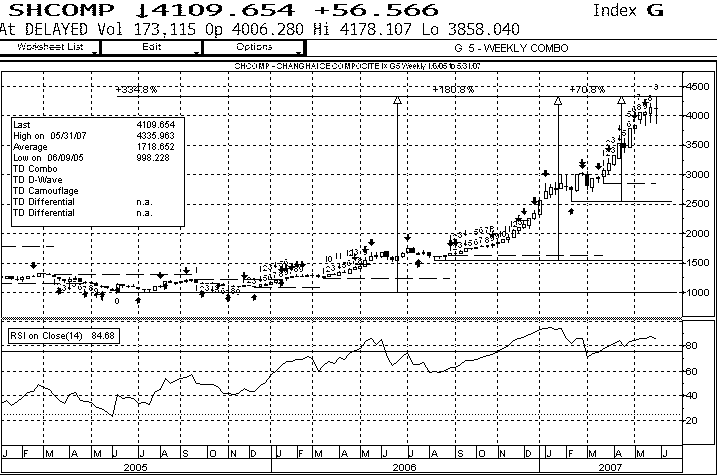

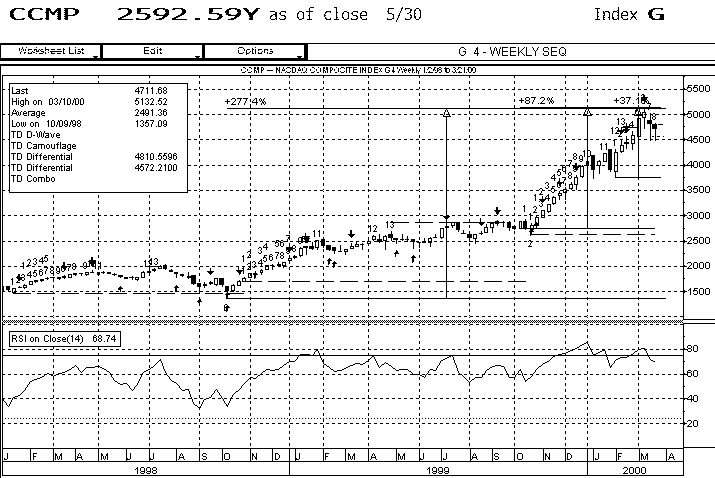

Use this handy-dandy checklist next time you think you see a price bubble forming and want to call a top. I’m going to look at the most over-exuberant market, the Shanghai Composite Index (DJSH) to see if the recent 180% run is getting a bit “extended.”

1. Parabolic Price Increase

1. Parabolic Price Increase

This one’s pretty obvious since parabolic price increases are the definition of a bubble. We’ve had so many examples of bubbles now that it’s getting pretty easy to spot the crazy price action that marks the final phases of a stock bubble advance. And all bubbles should be compared to the granddaddy of all bubbles – the NASDAQ from 1998 to 2000. The Shanghai’s parabolic advance looks very similar to the Big Nasdaq.

Amazingly, the current advance in Shanghai makes the NASDAQ blow-off look tame. Since the beginning of the move in 2005, the Shanghai has advanced 335% vs the 1998 – 2000 advance of the NASDAQ of 277%. The final acceleration higher in the NASDAQ from October 1999 to March 2000 went up 87%. The current blow off in Shanghai from September to today has registered a 180% increase. The current parabolic move in China is truly historic because, at the time, the NASDAQ bubble had been the biggest bubble move ever.

Here’s the three-year chart of the Shanghai composite…

Chart Courtesy Bloomberg

…versus the NASDAQ composite from 1998 to 2000.

Chart Courtesy Bloomberg

2. Strong Indexes Mask Underlying Weakness

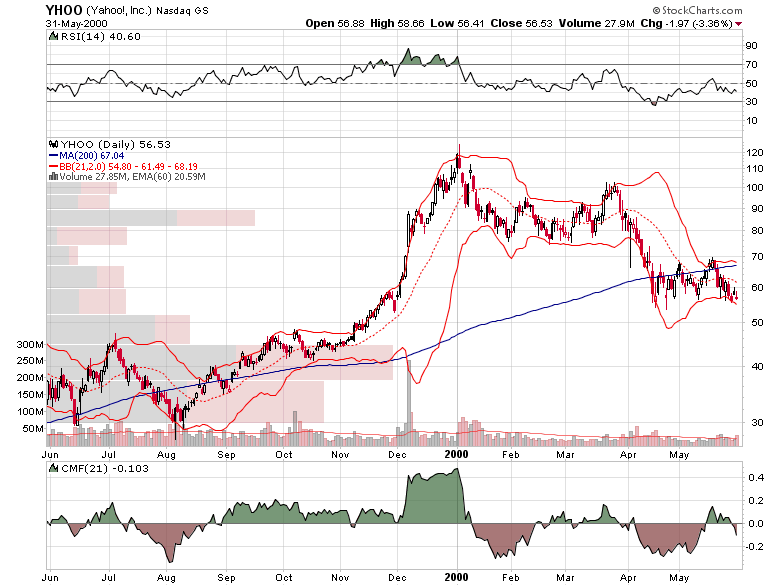

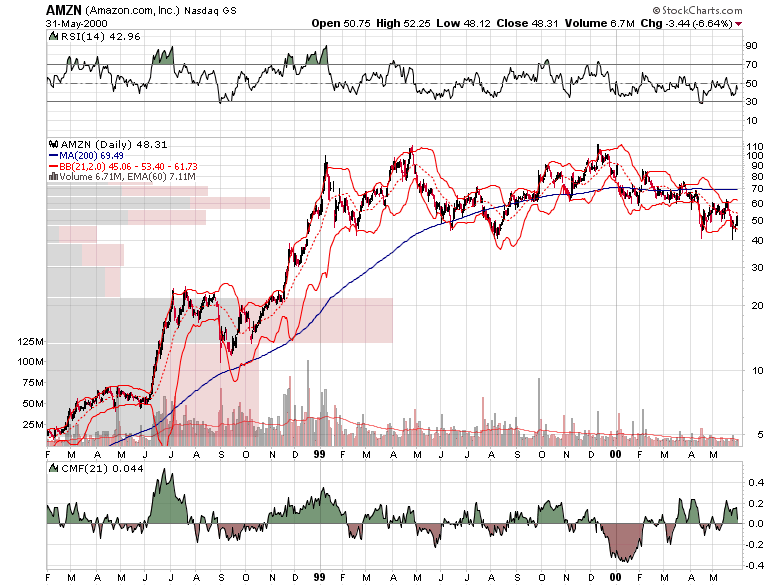

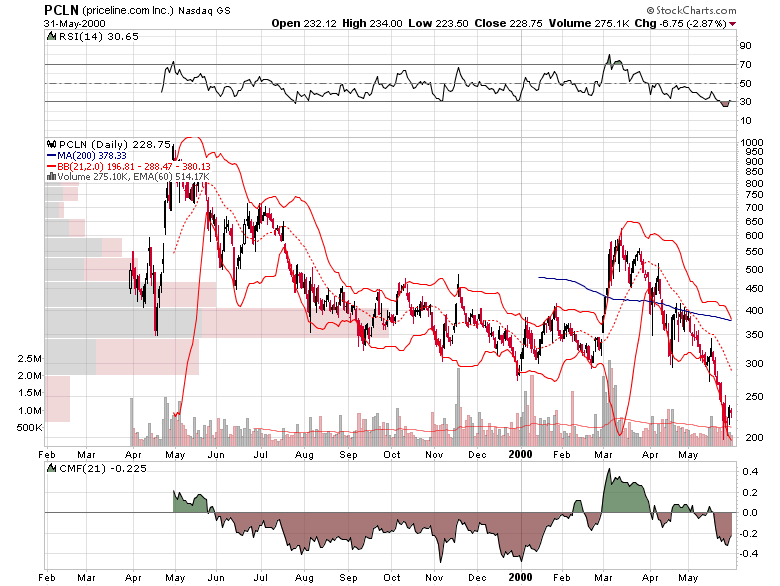

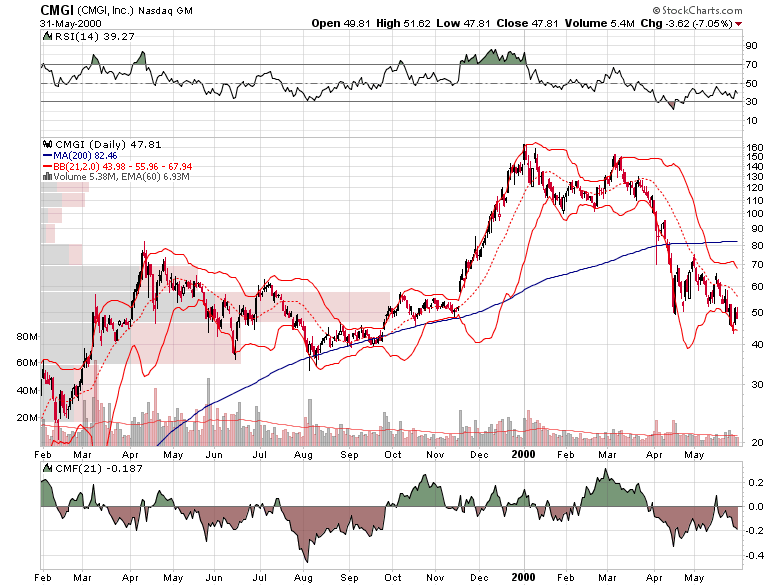

During the final stages of a bubble blow off, most stocks have already peaked out and are beginning to head down. Here’s a snapshot of some of the leading Internet stocks from 1999 to 2000. You’ll notice that none of them were hitting new highs with the NASDAQ in March 2000.

Here’s a snapshot of some leading China stocks right now.

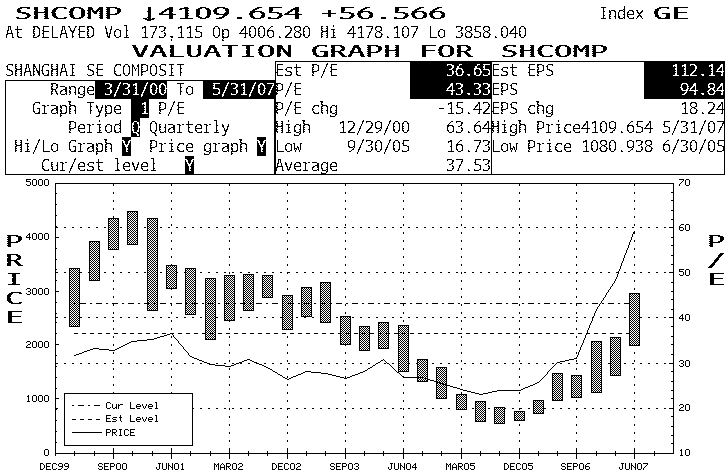

3. Valuations Are Off The Charts

In 2000, Cisco traded at 180x trailing earnings and 40x sales. Amazon traded at 100x sales and had no earnings. eBay traded at 1000x sales and had no earnings. In the Tokyo real estate bubble in the late 1980s, prime real estate went for as much as $100,000 a square foot. Now that’s a bubble valuation.

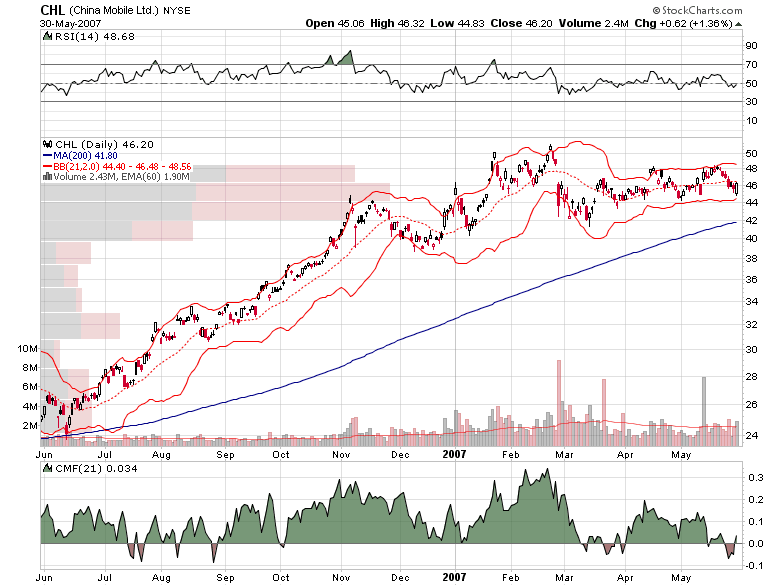

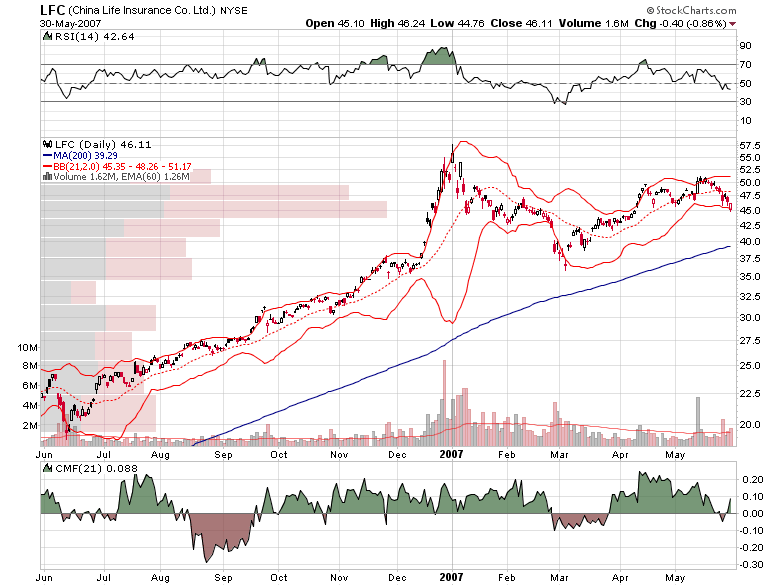

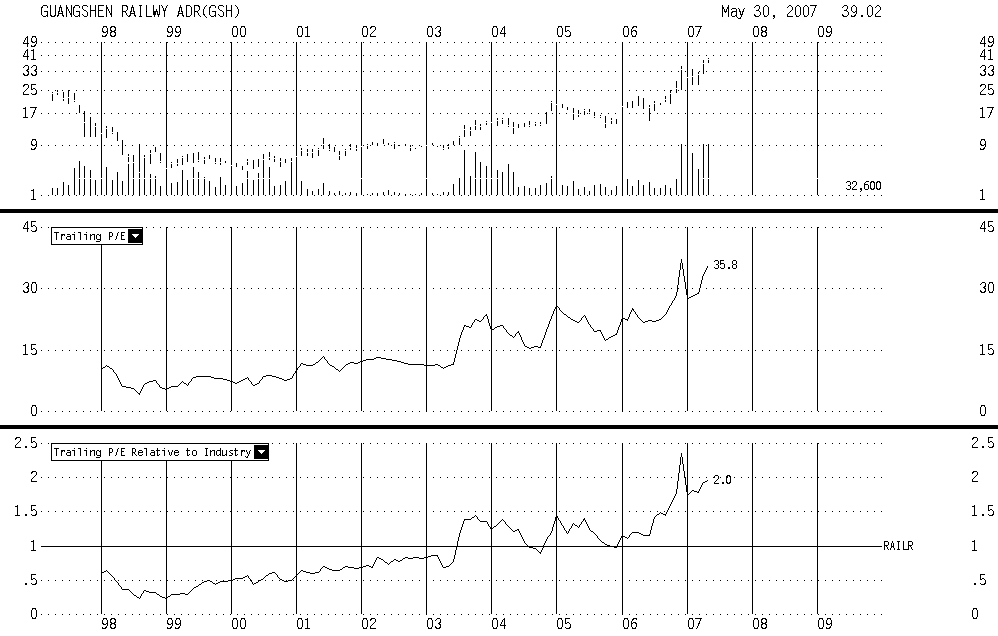

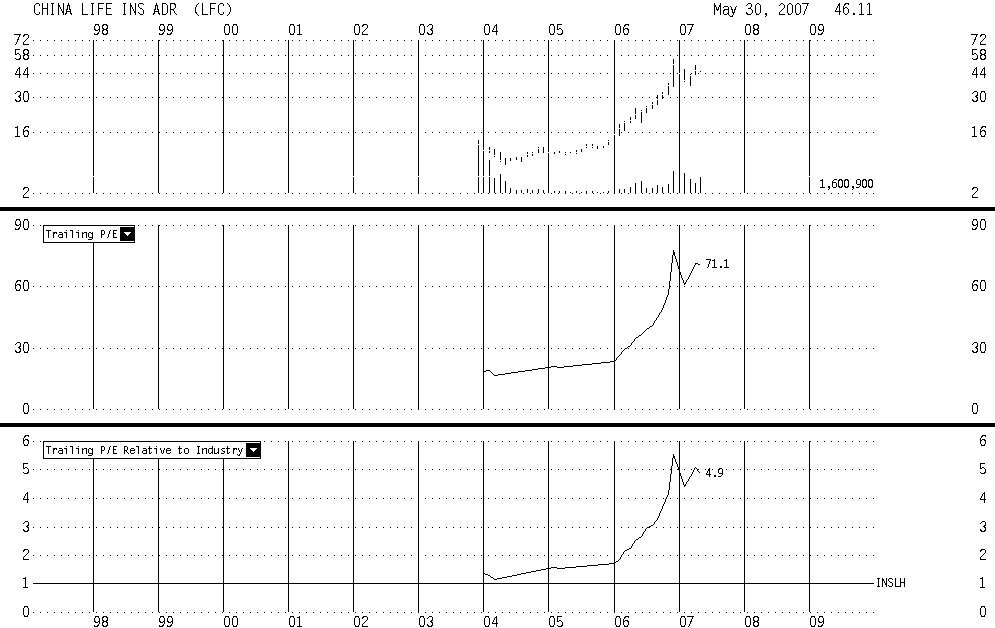

In comparison, many China stocks look downright cheap. While a couple of outliers like China Life (LFC) and Guangshen Railway (GSH) trade at well above average multiples and are approaching bubble valuations, many China stocks are simply trading at slight premiums to their industries.

China Life and Guangshen Railway look expensive…

Chart Courtesy Baseline

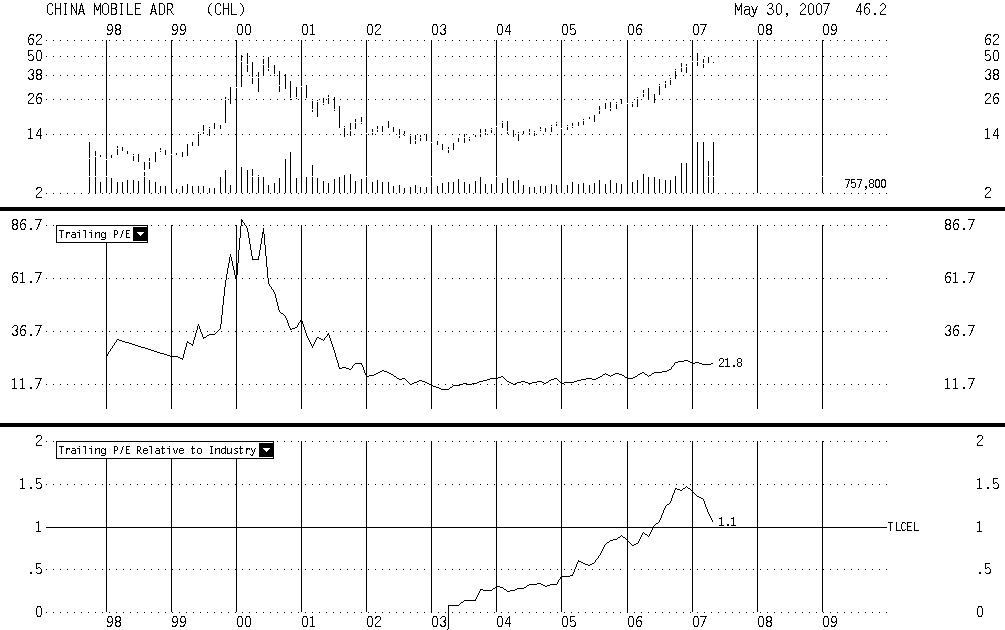

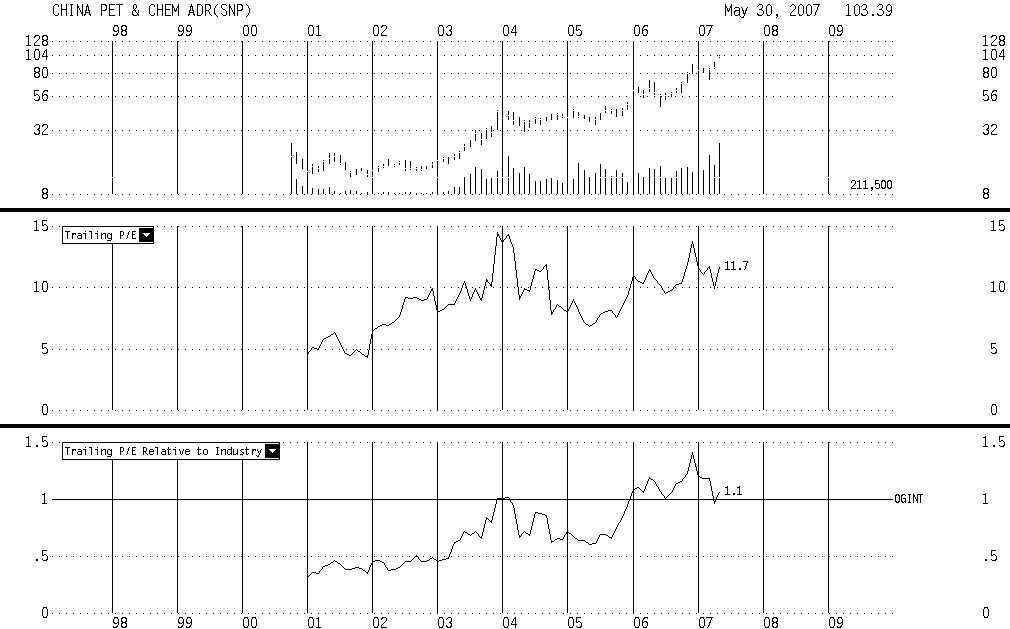

…but China Mobile (CHL), China Petroleum (SNP) and others are trading in line with their industry multiples despite the huge stock price advance.

Chart Courtesy Baseline

The overall Shanghai market is trading at about 43x earnings, which, while expensive, isn’t at the highest level ever.

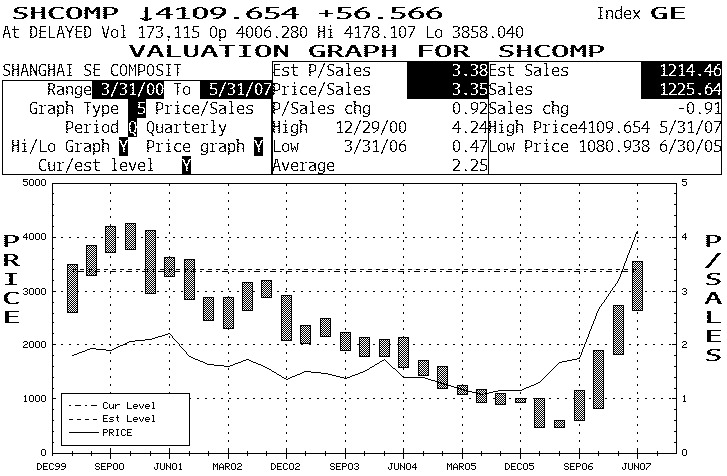

The price to sales ratio shows a similar pattern.

Chart Courtesy Bloomberg

4. Retail Investors Are All-In

In 1929, retail investors flocked to bucket shops to trade $200 of stock on $1 margin during their lunch hour.

In 1999, lawyers and doctors quit their jobs to trade stocks at day trading firms.

In 2007, Chinese are quitting their jobs to trade stocks. Over 27 million brokerage accounts have been opened in 2006 bring the total to well over 100 million.

From Chinadaily.com…

Xiao Feng, a former investment consultant at a futures company in Nanjing, put his three apartments and two vehicles – worth 5 million yuan – up as collateral days ago to get a 10 million yuan loan to invest in the stock market.

But the cost of borrowing is high – with an annual interest rate of 25 percent, he’ll have to pay the lender 2.5 million yuan in interest at the end of the year, reported the Nanjing Morning Post on Wednesday.

In addition, the lender will monitor his stock trading account. If the value of Xiao’s portfolio drops below 8 million yuan, the lender will liquidate his stock holdings to prevent a further decrease in the principal, spelling a loss of two million for Xiao.

When the 2.5-million interest payment is also taken into account, Xiao Feng will lose what he has worked for in the past 10 years – all his collateral.

Then why take such a risk? “Maybe it is the lure of the stock market. If an investment in a stock triples, or quadruples in a short period, then why not try?” he replied.

No wonder the Chinese government is so concerned. The road to capitalism will get much bumpier if people actually start getting a sense of risk and lose money. It will be an in vitiation for more, not less, government intervention – if that’s even possible in a communist country.

So, three out of four on the Bubble Top Checklist are definitely confirmed, and one is not. That’s probably close enough to call for a significant “correction”. Tomorrow, I’ll take a look at how US investors might be able to make some money off of the China stock bubble “correction”.

Nicely done. I agree that the big X valuations is inapplicable to some of the stocks that I follow. I have a list of the stocks in the Halter Index that I follow regularly and I have a small position in WZEN. What is “odd” (or interesting you could say) is the lack of market moving information. IN the US one can see this information rather quickly. But for C-stocks, it appears to not be instantaneous. I’ll point out the move in China Eastern Airlines as an example.

Not that I disagree with the above study, on the contrary. I just question whether we’re there yet.

I often try to see things from a different prospective to my view/opinion to see if I’m missing something. A contrarian hypothesis would be to look at simply the demand and supply for equities. The fact is that the mkt cap is tiny for an economy and population of the size of China. There just aren’t enough quoted stocks nor enough of them to go round. Last week alone 300,000 new brokerage accounts were opened and private investors are mortgaging their houses to participate in the rally. Whilst this undoubtedly signals a top, it may still have a long while to go. And just like in 1998 valuations were off the chart with Nasdaq stocks, the bull still had the energy to run for another 2 years. Ultimately, mkts revert to fundamentals but these can take a long time to materialise. The only thing that will cause the Chineses mkt to reverse will be their sentiment. If you read local reports, not only are they convinced that their country will regain the glory of yesteryears (and they will) but that their economy will keep powering ahead. With such conviction and momentum, it will take more than rate hikes or stamp duty to stop this train

This was a very interesting read. However, I disagree with the basic presumption that what happened in the past will happen again the same way. The gdp growth of China of about 10% for 30 years is a big factor in my disagreement. The middle class is growing, and with it come new retail investors- while many are jumping in, there is a lot of catching up to be done. Many companies are not even listed yet.

While I think the Chinese market is in fact due for some serious correcting, I doubt that 7 years later it will be so below the high mark as we currently are with nasdaq. In other words, I agree on a sharp pullback, but not really a prolonged downtrend like in nasdaq.

Meanwhile, I don’t invest in China because it seems too wild for me. I’ll wait until their markets are more mature even though it has been thousands of years to get to this point.

I had a lot of responses about this article so I thought I would clarify some of my thoughts.

I started looking at the Shanghai market after reading Robert Hsu’s excellent newsletter, China Strategy. He’s a well connected and intelligent analyst that actually has experience living and trading in Asia. His analysis is coherent and well researched. He wrote in the May 3rd issue …

“I’ve also heard stories of Buddhist monks becoming avid day-traders who visit local brokerage houses on a daily basis, wearing baseball caps to disguise their shaved scalps. The most interesting story to me involved hundreds of Shanghai nannies who quit their jobs last month to become full-time stock speculators. Everyone, it seems, wants a piece of the China Miracle.

The Chinese nanny story struck a personal chord with me because my childhood nanny in Taiwan, Miss Wu, recklessly plunged all of her personal savings into the Taiwanese stock market during the late ’80s. She managed to turn $60,000 into $300,000 by purchasing highflying bank stocks on margin. But when the market eventually crashed, Miss Wu lost everything. She had no retirement funds left, and my family has been helping her ever since.”

We’ve seen this thing over and over in the past decade. Unsophisticated investors drive up asset prices to unsustainable levels creating the risk for serious declines. Whether it be the NASDAQ, real estate, or whatever, it all ends the same way – when investors who don’t understand risk use margin and cheap money to chase exorbitant returns, it ends in a major collapse.

So if it looks like a duck, quacks like a duck and waddles like a duck, it’s probably a bubble.

I think the most compelling argument AGAINST a massive decline occurring is that 1) valuations aren’t absurd and 2) we are still in the early innings of the Shanghai market run-up.

The Shanghai market was in a serious slump just 18 months ago. So if we go back to my NASDAQ comparison, we might well be in 1997 or 1998, not 2000. From 1995 to 2000, the NASDAQ advanced 567%. The Nikkei in the 1980s, which was probably one of the top ten bubbles of all time, increased about 470% in the entire decade.

Part of the Shanghai advance is “catch-up” because of significant reforms taken on by the Chinese government. Prior to 2005, the best Chinese companies weren’t listed in Shanghai, they were listed in Hong Kong or on the NYSE. The Shanghai market was a dumping ground for virtually bankrupt State Owned Enterprises (SOEs). But recently, quality China companies like China Life, China Aluminum and Sinopec began listing their shares on the Shanghai Index. In addition, the Chinese securities regulators made all classes of shares tradable. That eliminated much of dual or triple ownership structure that made analysis of these SOEs virtually impossible. And the increased transparency lead to higher valuations.

But what worries me about the Shanghai market, is the speed of the advanced. The from 1995 to 1998, the NASDAQ advanced about 164% until it hit a 33% correction in 1998. In comparison, the Shanghai market has increased 330% in two years. That type of advance is unsustainable and will result in serious downside volatility. It might not spell the end of the bull market, but it will result in some breathtaking declines.

A second argument against a massive decline is that valuations of China stocks are not absurd. This is actually somewhat difficult to quantify because there are four different markets in China. In addition, many of the leading Chinese stocks are listed on markets outside of Shanghai.

While some shares trade at absurd valuations, some share trade at low valuations. China Life (LFC) at 73x earnings looks like a bubble valuation to me. But China Mobile (CHL) at 21x earnings looks reasonable. Cnooc (CEO) at 10x earnings looks cheap but CTRIP.COM (CTRP) at 76x earnings looks expensive. So as you see, you can’t paint the China market all with one brush, which makes it difficult to say that the valuations are too high.

Just one more note. The “strong fundamentals” argument is usually irrelevant in understanding bubbles. The fundamentals are always strong as bubbles form. It’s the strong fundamentals that creates excitment and increased stock speculation. Saying that internet companies were all money losing ventures is revisionist history. EBAY, AMZN, AOL, CSCO and YHOO were the fastest growing companies in the history of the world. Many are now the most profitable as well.

Investors create the bubble by projecting these strong fundametals to infinity. They then price the share with these absurd linear projections. That leads to massive overvaluation which creates the final phase of the bubble. When the speculation reaches an excessive levels, it bursts not because of poor fundamentals but because something changes investor behavior. An external shock, less liquidity or simple exhastion can all spell the end of the advance.

Therefore, I would expect a lot more serious declines on the order of 15% – 30% to shake out a lot of the new, retail investors. But I can’t say for certain that its the end of the run. Hence, my call for a “correction,” not a collapse in the Chinese market.

Literature is a kind of intellectual light which, like the light of the sun , may sometimes enable us to see what we do not like.

Thank God! Smoeone with brains speaks!

The road to capitalism will get much more bumpy if people actually start getting a sense of risk and lose money. It will be an in vitiation for more, not less, government intervention – if that’s even possible in a communist country

We will see this is likely to be an usaneanplt and bumpy ride. If there is no second suitor (as I suspect), and Sun’s board was doing the brinksmanship thing, then investors aren’t going to be too happy. If Sun continues on its own through its end of year in June, I am guessing we will see a significant shareholder throw the bums out reaction during the shareholder meeting. If (as Chris S suggests on the beowulf list) this is nothing more than board factionalization between Scott McNealy and JS, well, then Sun shareholders have quite a bit to worry about as the board wouldn’t be acting in the interests of the shareholders.

Harvey, I’ve got an equipment qiuetson for you. According to Esignal’s website, it only runs on PC. However I see you pulling up a Safari window briefly to show the time in New York and in the other video where you show your setup, it’s a small Macbook or Powerbook. My qiuetson is, how are you getting esignal to run on a Mac? VERY educational videos by the way!