“You can’t be a real country unless you have a beer and an airline – it helps if you some kind of a football team, or some nuclear weapons, but at the very least you need a beer”

— Frank Zappa

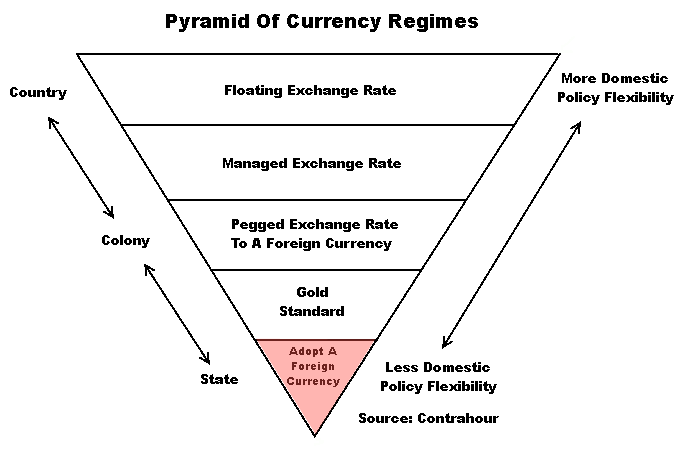

Every country definitely needs a good beer. But Frank Zappa missed one thing. Every independent country also needs its own currency. Without a sovereign currency, a country turns into nothing but a state or a colony, inexorably tied to the rules and policies of a foreign government.

We are living in an incredible era, where you can see in real life what happens when a country gives up its currency and turns into a state. It’s called the European Union. The European Union is made up of 28 countries. Nineteen of those countries have given up their currencies for the Euro. In essence, these nineteen countries have turned into states. This was the point, after all…to create “The United States of Europe.”

However, in doing so, the countries gave up something important…they gave up their domestic fiscal policy independence. In 2012, the EU countries adopted a conservative fiscal spending treaty which put government budgets under the careful eye of the central government in Brussels. Even though the EU countries have a vote in the European Union Parliament and still control their own central banks, for all intents and purposes, these become subservient to the fiscal demands of several large countries in the EU.

To take it a step further, the EU was first and foremost created around the idea of “price stability”. All countries in the EU admired the Deutsche Mark for its stability. In fact, before the Euro, the continent created the European Exchange Rate Mechanism (ERM) in which numerous currencies were essentially pegged to the value of the Deutsche Mark. So with the introduction of the Euro, Europe essentially adopted the Deutsche Mark as its currency. And with it, they adopted the fiscal policies of Germany.

In this regard, Europe has adopted one of the most extreme foreign currency regimes; nineteen nations in the EU have, de facto, adopted a foreign currency: the Deutsche Mark.

In this regard, Europe has adopted one of the most extreme foreign currency regimes; nineteen nations in the EU have, de facto, adopted a foreign currency: the Deutsche Mark.

Germany is an export-based economy with an ugly history with inflation, so its goal is maintaining currency stability at all cost. That means two things for the country and currency.

First, it means low levels of deficit spending. In “The Recipe for Inflation,” we mentioned that increased government spending can lead to inflation IF spending outpaces a country’s resources to supply the goods. Germans are notoriously conservative with government fiscal policy because they are constantly worried about stoking hyperinflation. German policymakers have therefore written these conservative spending rules into the EU treaties by imploring each country to run a balanced budget.

Second, Germany also exports a significant percentage of its industrial output, so it wants the value of the Euro to remain relatively low. To keep the Euro low, Germany has to keep inflation low. And to keep inflation low, the government has to limit consumer demand. So even though German citizens earn higher than average salaries, the government subjects citizens to higher than average taxes and social security payments. This limits consumption and decreases the demand for imports.

Germans, by their upbringing, view themselves as a rather frugal tribe. But this is not an accident. The German government imposes frugality on its citizens through its tax policies to limit consumer demand, keep inflation low and exports high.

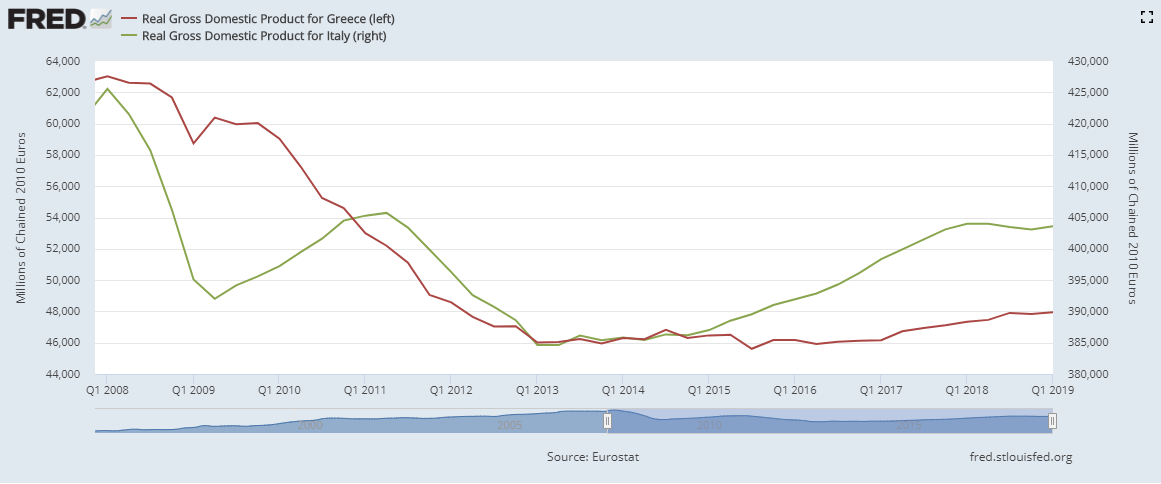

With the establishment of the EU, Germany has exported its frugality. While joining the EU gave countries more credibility in international trade and lowered borrowing costs, many countries are suffering at the expense of domestic policy flexibility. Countries that rely on other industries besides manufacturing, like Italy and Greece, hate the Euro because they need more domestic spending to improve their economies. The fiscal spending restraints are suffocating them.

The 19 European countries that have officially adopted the Euro have truly become states. These governments have given up their ability to regulate their domestic spending for the benefit of having easy access to international markets and financing. However, if these countries do not run a trade surplus, the benefits are negligible. Just like the individual states in America, these 19 European countries cannot print their own currency, cannot run budget deficits for long before hitting borrowing constraints, and cannot regulate trade.

The irony is that even the Germans realize their spending constraints are absurd. The constraints don’t allow governments to react to economic downturns. During the recession of 2003, both Germany and France broke the official government spending constraints. This led the head of the European Union Commission to say “I know very well that the stability pact is stupid, like all rigid decisions.”

Like everything in the world, the solutions are easy but the execution is difficult. The solution would be to allow the EU countries greater flexibility in budgeting. Rather than running balanced budgets, the EU could allow individual countries to run budget deficits of 5%-10% if they prove that inflation hasn’t increased materially. This solution would give countries without a trade surplus enough flexibility to manage their economies. But such a political solution seems unlikely until the next crisis erupts and threatens to break the EU apart.

By turning themselves into states of the European Union, the countries of Europe have given up their domestic policy flexibility. And while these countries have their own flag, their own beer, and their own football team, it is a country’s own currency that determines its sovereignty.

So, here’s hoping that Germany figures this out before it tears the European Union apart.

Prost!

Over the next several posts, I’ll take a look at examples of different exchange rate regimes countries adopt and the effect that has on domestic monetary and fiscal policy.

Everything You Know About Economics Is Wrong: How Soros Broke The Bank Of England