Truth is borne from extremes.

Nothing is more extreme than depression or war. This is how, in the aftermath of The Great Recession, I came to understand that everything I knew about money was wrong.

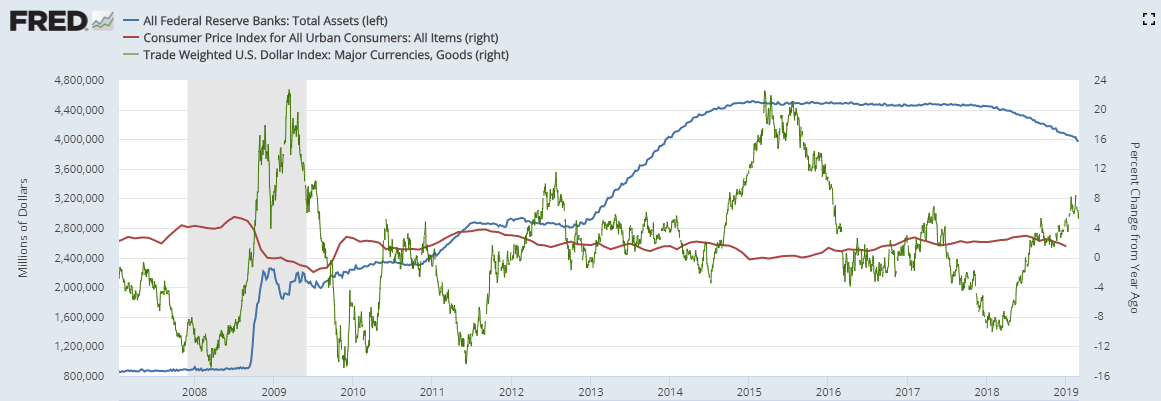

Everything I learned about economics up to that point said: if the Federal Reserve monetized the national debt by printing money, it would create inflation and the US dollar would decline.

However, the exact opposite happened. Inflation went down. The dollar went up.

All the economic experts were wrong.

It turns out, they were all using the wrong theories. They were trying to bake a cake using instructions from Ikea.

Time and time again, central bankers across the US, Europe, and Asia have lamented about their inability to generate economic growth and inflation.

Over the past decade, most of the economic updates went something like this from Britain’s Central Bank in 2018:

The Bank of England has put back plans for an increase in interest rates after the weaker-than-expected performance of the economy in early 2018.

Although the Bank believes the soft patch in growth will prove temporary, seven of the nine members of its monetary policy committee adopted a wait-and-see approach to raising official borrowing costs and voted to keep them at 0.5%.

The Bank’s decision – which was outlined in its quarterly inflation report – will come as no surprise to the City, which expected Threadneedle Street to ditch plans for tighter policy this month in the light of first quarter growth of 0.1%, a faster-than-expected fall in inflation and evidence that consumers were cutting back on spending.

And central bankers will continue to be ineffective at generating inflation until they realize they have the wrong recipe. Conventional wisdom states that central bankers print money. But they do not. Central bankers can only affect monetary policy. All they can do is move the dial on the level of interest rates.

The government, however, can print money. This is referred to as fiscal policy. The power of fiscal policy dwarfs the power of monetary policy. During normal economic times, this dynamic isn’t apparent because typically, governments increase spending steadily from one year to the next. Government employees receive automatic pay raises, military budgets increase, and legislators don’t feel much pressure to change.

In a normal environment, making minor adjustments to interest rates allows central bankers to manage the economy.

During times of crisis, however, fiscal policy decisions get made that can destroy entire countries.

After the Greek Sovereign Debt crisis, Europe followed a path of fiscal austerity. Instead of expanding government spending, the European Union doubled down on debt reduction by signing the Treaty on Stability in the Economic and Monetary Union. This treaty limited governments to running budget deficits of no more than 3% of GDP.

Despite European Central Bank Chairman Mario Draghi’s best efforts, Europe has barely recovered from imposing these government spending limits. Draghi jacked up the Central Bank’s balance sheet, helping get GDP growth to slightly over 2%. However, growth has tailed off considerably.

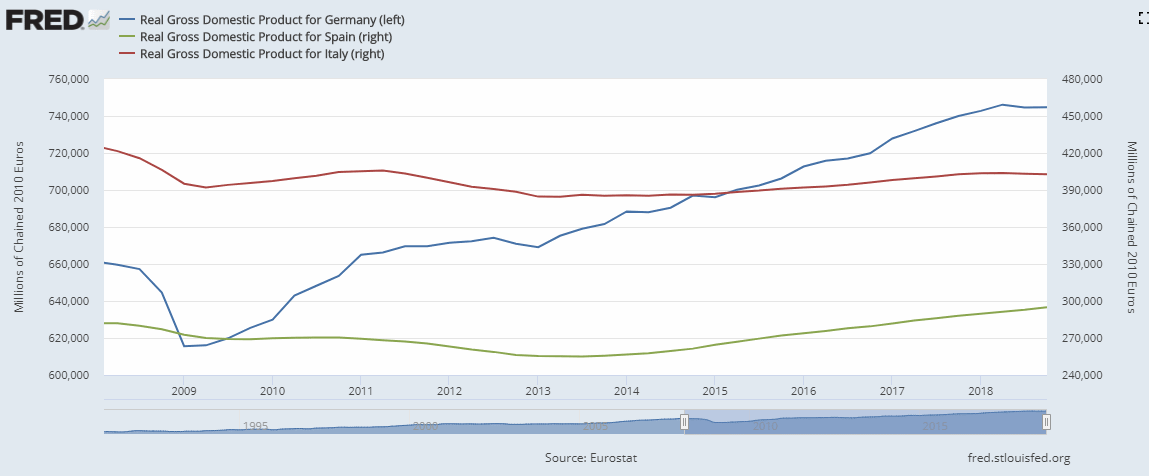

In addition, Draghi’s efforts have had virtually no effect in countries that do not run big current account surpluses like Germany. Spain’s and Italy’s economies have not grown at all in the past ten years.

And Spain and Italy won’t experience any growth until the leaders of Europe get the correct recipe.

The cookbook for fighting an economic downturn was actually written in Japan in the 1920s. Korekiyo Takahashi, five-time Japanese Finance Minister, wrote it. After a series of banking crises in the 1920s and a disastrous return to the gold standard in 1930, Takahashi was called in at the ripe age of seventy-seven to fix Japan’s economic ills.

Takahashi’s formula was simple. He instantly reversed the contractionary economic policies with three new initiatives:

- He abandoned the gold standard and devalued the Yen to improve exports (exchange rate policy);

- He lowered interest rates (monetary policy); and

- He increased the government deficit (fiscal policy)

First, the devalued Yen created a fertile environment for export growth:

The result was a dramatic rise in Japanese exports of goods and services both in nominal and real terms. Nominal exports, which had dropped by 25 percent in 1930 and 16 percent in 1931, rose by 22 percent in 1932 and 25 percent in 1933. (From Japan’s Recovery from the Great Depression)

Second, the Bank of Japan conducted an accommodative monetary policy by cutting its official discount rate in March, June, and August 1932.

Finally and most importantly, Japan’s government increased deficit spending providing a stimulative fiscal policy. Before Takahashi became Finance Minister, the Japanese government only ran a deficit for specific purposes, such as public works, reconstruction, or war. Under Takahashi, funds were used for all general government expenditures. For instance, Japan’s 1932 budget included emergency relief programs for rural areas affected by crop failures.

By 1932, Takahashi’s interventionist policies had reversed Japan’s economic decline. After growing just 1.1 and 0.4 in 1930 and 1931, Japan’s economy grew an average of 5.8 percent from 1932 onwards.

Takahashi masterful understanding of the economy also included the consequences of his stimulative policies:

Takahashi, however, understood that financing government expenditures by issuing debt was limited by the ability of the public to absorb it. Beyond that, it becomes inflationary. In Takahashi’s words, ” the limit comes when the effect of the additional funds raised by issuing debt has no value in fostering private industry and, therefore, no stimulus on sound development” (1936a, pp. 54-55.) He saw this limit being reached in 1935 when he made the fatal decision to attempt to rein in military spending. (From Japan’s Recovery from the Great Depression)

Unfortunately, his understanding of how to slow economic growth also lead to his death. After cutting the military budget in 1935 to keep from stoking inflation, Takahashi was assassinated by a group of militarists on February 26, 1936. The budget deficits continued unabated and inflation spiked.

Takahashi was a master finance minister. He understood one hundred years ago what European finance ministers still don’t know today: the recipe for economic growth is an increase in fiscal policy, an expansionary monetary policy and a depreciating exchange rate policy.

https://contrahour.com/2019/04/everything-you-know-about-money-is-wrong-the-us-wont-turn-into-the-wiemar-republic.html

1 thought on “Everything You Know About Economics Is Wrong: The Recipe For Inflation”

Comments are closed.