Japan is a real-world example that shows traditional macroeconomic theory is wrong. Every myth that you have heard about government “printing money” breaks when you examine Japan’s economy.

Typical commentary from economists or investors will go something like this from Asian investor Peter Pham:

Japan in Debt and Danger

Japan currently has such a high level of debt that it’s doubtful the country can ever repay the full amount.

To know more about the complexity and seriousness of Japan’s debt predicament, we have to understand how the government pays for its commitments and public services annually.

In all economies, governments fund public services by levying tax to its citizens.

If total tax revenue exceeds public services costs, then there is a fund surplus. However, if the total amount of tax is less than government spending requirements, then is a fund deficit, and the government has to figure out how to cover this loss by borrowing.

To make up for this deficit, governments issue bonds, or IOUs, and sell them to investors along with paying interest. If the level of debt is small relative to tax revenues, the interest payment has a small value. But once the government borrows a higher amount, national debt level increases, and thus investors become more concerned over the risk of default.

The higher the risk of default, the higher the bond interest rate – the additional amount that covers the added risk for investors.

To lower the burden of debt, Japan’s central bank reduces the interest rate and purchases government bonds to supply the financial system with more cash. Theoretically, this artificially minimizes the total interest repayment.

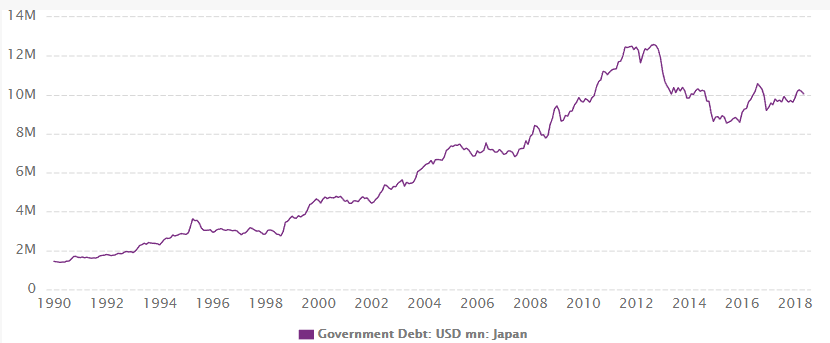

Because the Japanese government’s debt is so high, the interest expense can easily be affected by rate increases. In fact, Japan’s debt was 15 times higher than the tax revenue collected by the government in the end of 2016.

Based on this trend, we can figure out when the government will not have enough tax revenue to cover interest payments. By 2041, assuming tax revenue remains constant and there won’t be any economic shocks, Japan’s interest repayments will exceed tax income.

To provide more attractive debt options, the government will have to tolerate more interest liabilities. That means increased loaning to pay for this.

This is a typical perpetual debt trap, a vicious cycle where borrowing to service an ever-growing interest repayment. The more you’re borrowing to pay debts today, the more interest and obligations you’ll have to face tomorrow.

Japan may be a prodigal debt manager for now, but because the structure of its society will not change significantly and its economy is not productive enough, the only viable option is default.

This scenario is what economist claim to be impossible. Unless Japan attempts a leap of fate to ensure economic grow outpaces interest payments, then the die is cast.

None of this will happen since it is built on a faulty understanding of national debt. Japan will not go bankrupt because taxes are not how a government finances itself. Interest rates will not spike to unsustainable levels because they are set by the Bank of Japan.

In fact, any close examination of Japan’s economy shows everything you think you know about the country is false.

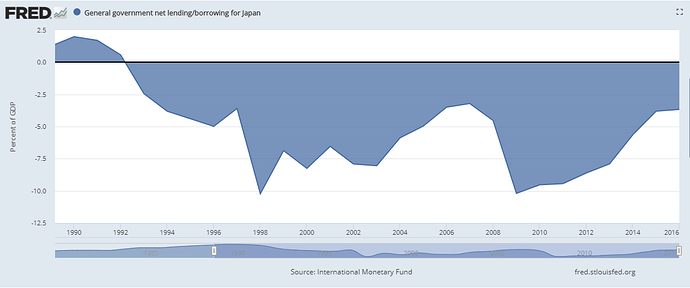

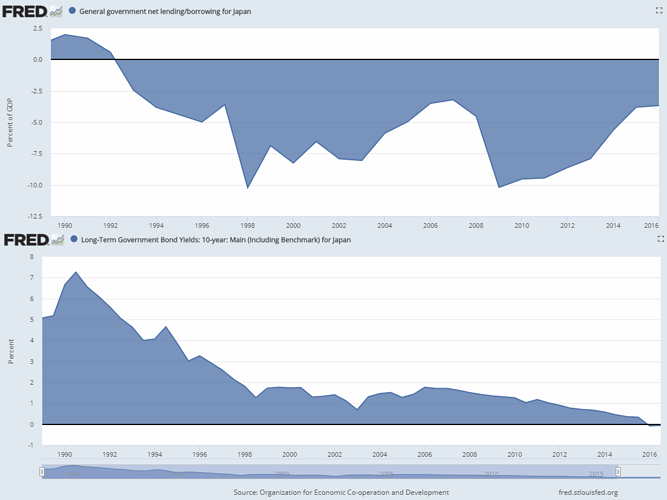

First off, Japan has been running massive government deficits for the past 25 years. Ever since 1992, the government has spent more money than it has taken in.

This “money printing” should lead to inflation according to traditional macroeconomic theories. But the government always prints money to pay for things its citizens need. Money printing doesn’t lead to inflation because as long as the government is drawing on resources available to it, prices won’t rise. Only if the government draws on resources unavailable to the country does inflation rise.

This is clearly seen in Japan. Even though the government has been running budget deficits, Japan has been fighting deflation for the majority of the past 25 years. Inflation hasn’t risen over 2% over that timespan.

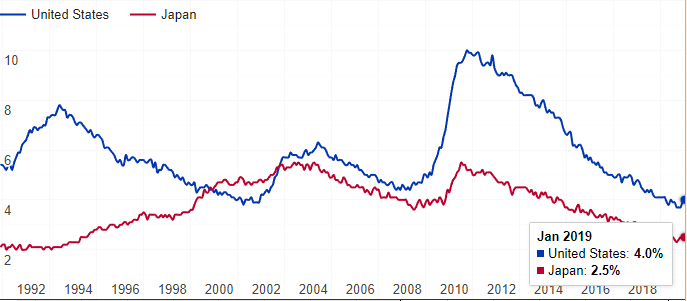

You would also think that if the government was printing so much money, interest rates would skyrocket. The market would demand a higher interest rate because investors would fear a government default.

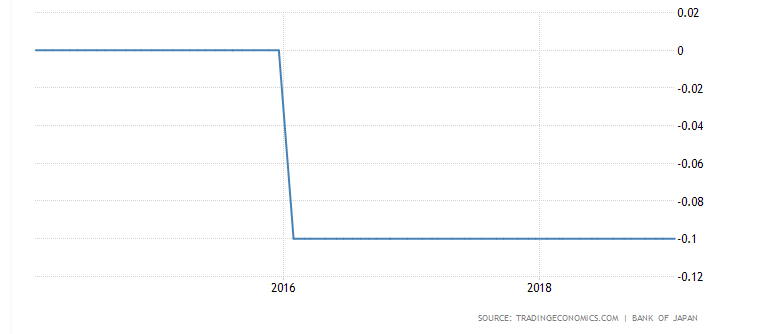

But that isn’t the case either. Ten-year interest rates are currently 0% in Japan. The market isn’t demanding a higher interest rate because it understands Japan does not have any default risk. A government that controls its own sovereign currency can never go bankrupt.

In addition, unlike what traditional economic theory would tell you, the Central Bank, not the market, sets short-term interest rates. Interest rates are just a monetary policy tool used by the central bank to try to manage the economy and inflation.

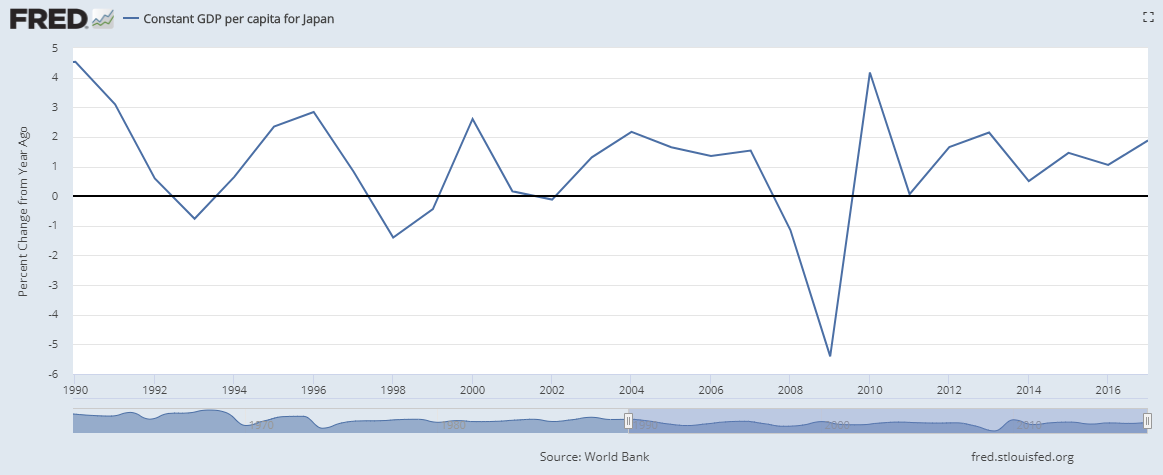

Classic macroeconomists will always reply to these facts with a “Yes, but look at Japan’s weak growth rate.” It is true that Japan’s economy hasn’t experienced strong growth in decades. If you listened to most economists, you would think the country is in shambles. But that is also wrong. Traditional macroeconomic theory can’t explain Japan so they point to the weak GDP growth as a sign that the country’s policies are failing.

Japan’s growth hasn’t actually been that bad if you look at it on a per capita basis. The country’s low growth rate is symptomatic of a low birth rate. But productivity and per capita GDP continues to increase. Despite the consternation about weak economic growth, Japan’s per capita GDP has actually grown at an average of over 1.0% during the past 20 years. Not blistering, but far from a disaster.

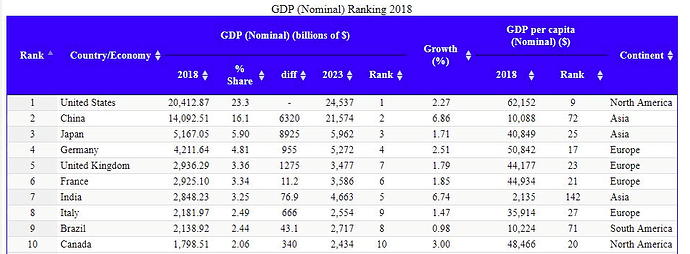

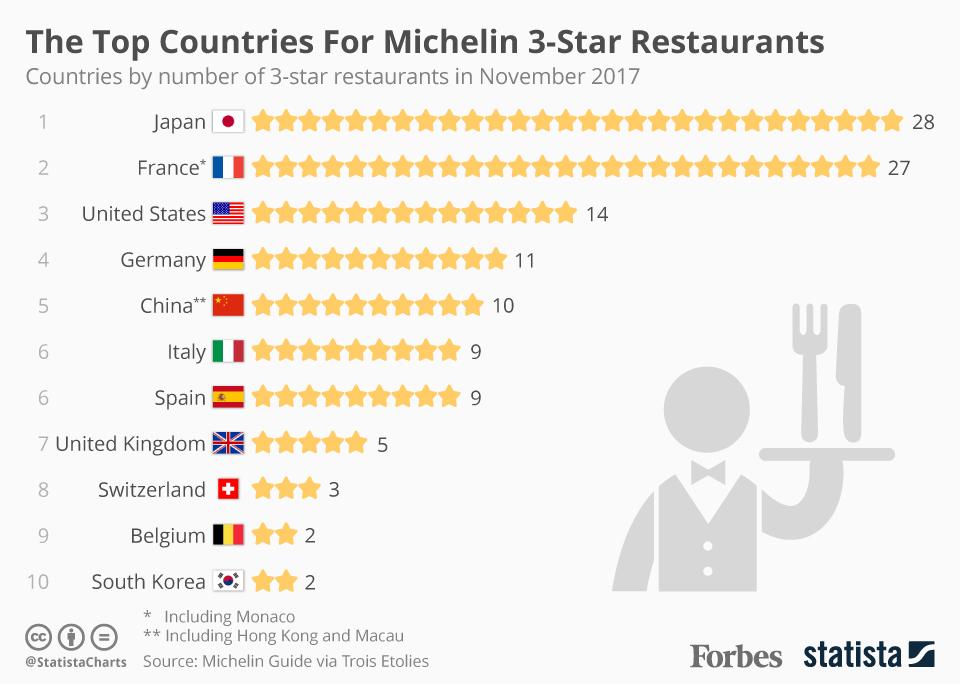

Step back a minute and take a look at the bigger picture. Japan is actually an economic miracle. Here is a country that was destroyed in 1945 that is now the world’s third-largest economy. Japan is an island with no natural resources which has the world’s second-best education system, the world’s second-longest life expectancy, and has had less than 5% unemployment for the past 10 years with rising productivity and rising per capita GDP.

Japan, an island nation with only 126 million citizens, has the world’s third-largest economy.

Japan has the second-best educational system. The United States isn’t even in the top 10.

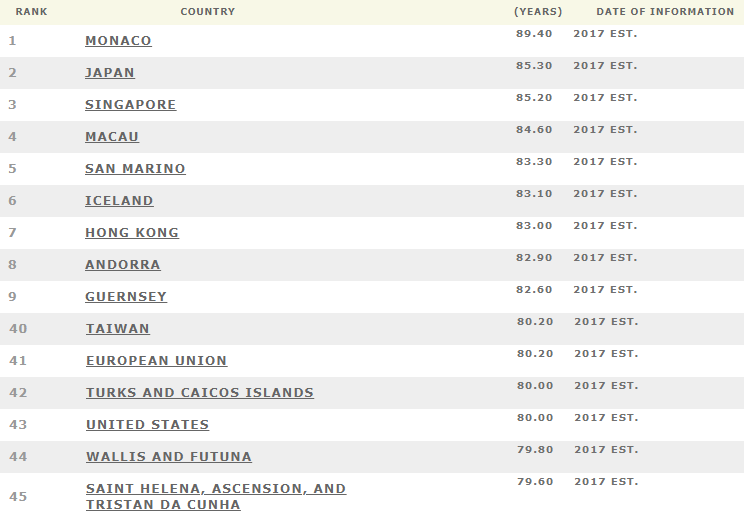

Japan’s average life expectancy at birth grew by 5 years to 85.0 years in 2017. This means the Japanese now typically live 5 years longer than Americans.

Even during the Great Recession, Japan’s unemployment rate only increased to 5.5% compared to over 10% for the US. Currently, Japan’s unemployment rate is near all-time lows.

The vast majority of Americans think Japan is fading into the sunset. Its population is declining, its economy is not growing much or at all and it has been eclipsed by China. I’ve argued for decades that that line of analysis is overstated. Japan is one of the world’s most advanced societies and maintains a very high standard of living.

I have been traveling to Japan since 1979 when I covered the Group of 7 meeting of world leaders, the first time it was held in Tokyo. Then in 1989, I spent months in Japan writing my book, The Japanese Power Game. During this sweep of 35 years or so, and over the course of dozens of visits, I have seen the Japanese transform their cities and build an incredibly extensive, modern transportation system. Their technology base is strong.

So, by way of a real-world example, Japan’s existence repudiates the myths of traditional macroeconomic theory. It is impossible to believe in the “sound money” philosophy and likewise live in a world that includes Japan. The idea that you can print money to the tune of 230% of GDP, while suffering through deflation, is incompatible with the idea that fiat money expansion will cause inflation.

To explain the existence of Japan, economists will often come up with new economic theories. Richard Koo, economist at Nomura Securities, made up a new term to describe what he saw in Japan. He coined the term “Balance Sheet Recession” to explain how Japan could run massive deficits without a commensurate increase in interest rates or inflation. However, if you actually understand that sovereign governments don’t finance their spending through debt issuance, you don’t need any new theories. And you certainly don’t need to duct tape your economic models together to explain the existence of Japan.

Most economists are such staunch advocates of laissez-faire that they reflexively dismiss Japan’s economic system. The only way they can deal with Japan is to call it a “failure.” But as any visitor to the country will attest, Japan is far from a failure. Japan is a country with one of the world’s most advanced economies, a strong culture, and a very high standard of living. Understanding how governments finance themselves has helped Japan improve citizen’s access to infrastructure, healthcare, and education systems.

Everything You Know About Economics Is Wrong: The Recipe For Inflation